Most people spend decades optimizing their retirement savings — maxing 401(k)s, timing Social Security, minimizing withdrawals. Then they turn 65 and get a Medicare bill they never saw coming: IRMAA, a surcharge that can add thousands a year in premiums for high earners.

But for someone with a seven-figure pretax IRA, focusing too hard on avoiding IRMAA can quietly cost hundreds of thousands in lifetime tax. Here's what IRMAA is, where the conventional advice around it falls apart, and how to think about Roth conversions strategically as you enter retirement.

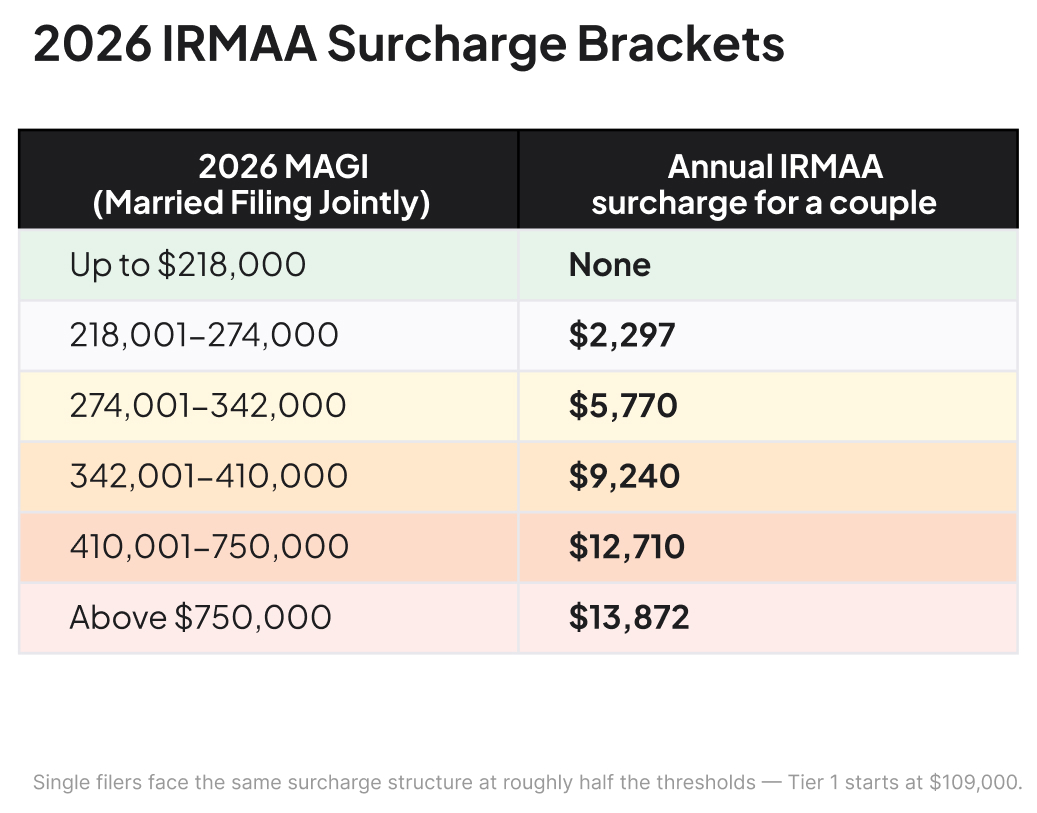

What Is IRMAA? The Medicare Surcharge Many Retirees Don't See Coming

IRMAA (short for Income-Related Monthly Adjustment Amount) is a Medicare surcharge added to your Part B and Part D premiums once your income crosses certain thresholds. It starts at age 65 and uses your income from two years prior — so your 2026 Medicare premium is set by your 2024 tax return.

The brackets are a cliff, not a slope: a single dollar over a threshold triggers the entire next tier. For a married couple filing jointly in 2026:

Why "Just Stay Below the IRMAA Threshold" Is Often the Wrong Advice

The most common online advice is to "size your Roth conversions to stay below the next IRMAA tier." For the average retiree, that's reasonable. For someone with a seven-figure pretax balance aiming to build Roth assets before RMDs begin, it's a framework that quietly costs more the longer you follow it.

The reason comes down to two very different questions:

"How do I keep my near-term tax bill as small as possible?" Stay below the next IRMAA threshold. The table above shows that avoiding the cliff can mean real savings.

"How do I pay the least tax over the rest of my life?" This requires a holistic view across your entire lifetime — Federal tax, state tax, IRMAA, and the eventual tax bill your heirs will face. The Roth conversion you skip this year to avoid IRMAA in early retirement can reappear later as a larger Medicare surcharge and a larger RMD, because the pretax IRA kept growing.

Why Many High Earners Should Convert Aggressively, Despite IRMAA

What a $3 Million IRA Looks Like at Age 75 If You Never Convert

A $3 million pretax IRA at age 65, untouched at 7% growth, becomes roughly $5.9 million by age 75. First-year RMDs of about $240K combined with Social Security put the couple in IRMAA Tier 2 immediately, and the surcharge climbs as RMDs grow each year. By the mid-80s, most couples in this scenario are paying at least Tier 3 or Tier 4 every year. Paying IRMAA for a few years of aggressive conversion is often far cheaper than paying it on RMDs for the next 20+ years.

The Widow's Penalty: One of Retirement's Costliest Surprises

When one spouse dies, the survivor files as a single taxpayer the following year, and the math shifts significantly. IRMAA Tier 1 drops from $218K (MFJ) to $109K (single). The 22% federal bracket compresses from roughly $206K to $103K, and the standard deduction roughly halves. The same retirement income that sat comfortably below the surcharge as a couple can push the survivor two tiers higher overnight. Roth conversions during the joint years when tax brackets are wider are one of the few tools that address this.

The Inherited IRA Problem Your Kids Don't Know About Yet

Under the SECURE Act, most non-spouse beneficiaries must deplete an inherited IRA within 10 years. An adult child inheriting a significant pretax IRA balance during their peak earning years will be forced to pull those distributions on top of their salary, potentially pushing them into the highest federal brackets for a decade. A Roth conversion today eliminates that problem entirely: the 10-year rule still applies, but inherited Roth IRA distributions remain tax-free.

When IRMAA Optimization Is the Right Strategy

There are real situations where sizing conversions to stay below a threshold is the right call:

- Limited cash outside the IRA. If the conversion tax has to come from the IRA itself, the break-even math weakens.

- A planned move to a lower-tax state. Conversions on the no-tax side of a New York-to-Florida move are significantly cheaper. The bulk of your conversion plan likely belongs on the other side of that move.

- Significant charitable plans. Qualified Charitable Distributions, sent straight from the IRA to a charity after age 70.5, never appear as income and count against RMDs. For the giving portion of the portfolio, conversions aren't needed.

- A modest pretax balance. Under ~$600K in pretax accounts, RMDs likely won't meaningfully disrupt your income, and the lifetime-tax case for aggressive conversion is weaker.

In these cases, it makes sense to be precise about the IRMAA cliff and convert up to (but not over) the next tier.

The Bottom Line: Minimize Lifetime Tax, Not Just Next Year's Medicare Premium

IRMAA is a real cost. It shouldn't be ignored. But optimizing exclusively around it at the expense of a larger Roth conversion strategy often costs more over a decades-long retirement than it saves.

The right framework: model the full picture. What do RMDs look like at 75 and 80? What's the widow's tax exposure? What does the inheritance look like for heirs? IRMAA is one input in that model, not the answer. Saving a few thousand on IRMAA in any one year can easily become hundreds of thousands more in lifetime tax.

Frequently Asked Questions About IRMAA and Roth Conversions

Does a Roth conversion count as income for IRMAA?

Yes. The converted amount is added to your MAGI in the year of conversion and counts toward IRMAA bracket determination. Roth conversions done before age 63 typically don't affect Medicare premiums, as the two-year lookback hasn't reached Medicare eligibility yet.

How does the two-year lookback rule work for IRMAA?

Medicare uses your MAGI from two years prior to set your current-year surcharge. Your 2026 Part B premium is based on your 2024 tax return. For someone who retires at 63 and reduces income immediately, IRMAA may still apply at 65 based on higher pre-retirement earnings.

Can you appeal an IRMAA determination?

Yes. If your income has dropped significantly due to a "life-changing event" — retirement, divorce, death of a spouse, reduction in work hours — you can file Form SSA-44 with the Social Security Administration to request a reassessment using more recent income data.

Is there an IRMAA income cliff to avoid?

Yes — the thresholds are hard cliffs. One dollar over the line triggers the full surcharge for the next tier. For a married couple, the jump to Tier 1 in 2026 costs $2,297/year. Strategic income management in the two years prior to Medicare eligibility can meaningfully reduce this exposure.

At what income does IRMAA start in 2026?

For married couples filing jointly, IRMAA begins above $218,000 in MAGI. For single filers, it begins above $109,000. These thresholds are inflation-adjusted annually.

Should I do Roth conversions before or after age 65 to avoid IRMAA?

Conversions completed before age 63 generally won't affect Medicare premiums, since the two-year lookback doesn't reach back that far. The window between retirement (often 60–63) and Medicare eligibility (65) can be an ideal time for aggressive Roth conversions without triggering IRMAA.

Is it ever worth paying IRMAA on purpose?

Yes. For high earners with large pretax balances, paying IRMAA to facilitate aggressive Roth conversion is often far cheaper than letting the pretax balance grow into much larger RMDs at age 75+, which usually means higher IRMAA tiers for the rest of retirement.

Disclosures:

The information contained in this communication is for informational purposes only. This content may not be relied on in any manner as specific legal, tax, regulatory, or investment advice. While we strive to present accurate and timely content, tax laws and regulations are subject to change, and individual circumstances can vary. Range does not make any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein. Range Advisory, LLC and Range Tax, LLC are wholly owned subsidiaries of Range Finance, Inc (“Range”). Tax services are provided by Range Tax, LLC. Investment advisory services are provided by Range Advisory, LLC. Range Advisory, LLC is an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Fees and additional information can be found at www.range.com. All investing involves risk, including the possible loss of money you invest.

You should not rely solely on the information contained here when making decisions regarding your taxes or financial situation. We strongly recommend consulting with a certified tax professional, accountant, or legal advisor to address your specific needs and ensure compliance with applicable laws.

.svg)

.svg)

.svg)