After eight years under Jerome Powell and more than a decade of a Fed that prized transparency above almost everything else, Kevin Warsh's first meeting as Chair was a genuine changing of the guard.

And he made sure you felt it.

Less hand-holding, a deliberately “curt” statement, and an unmistakable message that the Fed is still in the inflation-fighting business. Markets have reacted accordingly. Short-term rates are up, the dollar has firmed, and stocks have slid as investors hurry to reprice a Fed that suddenly looks less accommodating and less predictable.

%201.jpg)

The narrative has written itself. The financial press has its story: a hawkish new sheriff is in town. But look closer, and most of what feels new turns out to be pretty old. Strip away the novelty of a new face, and three things come into focus:

- New chairs almost always open in a stern, “hawkish” way

- The Fed used to talk far less than we've grown accustomed to

- Markets can do just fine under very different Fed chairs, so long as the Fed stays credible

New chairs come in swinging

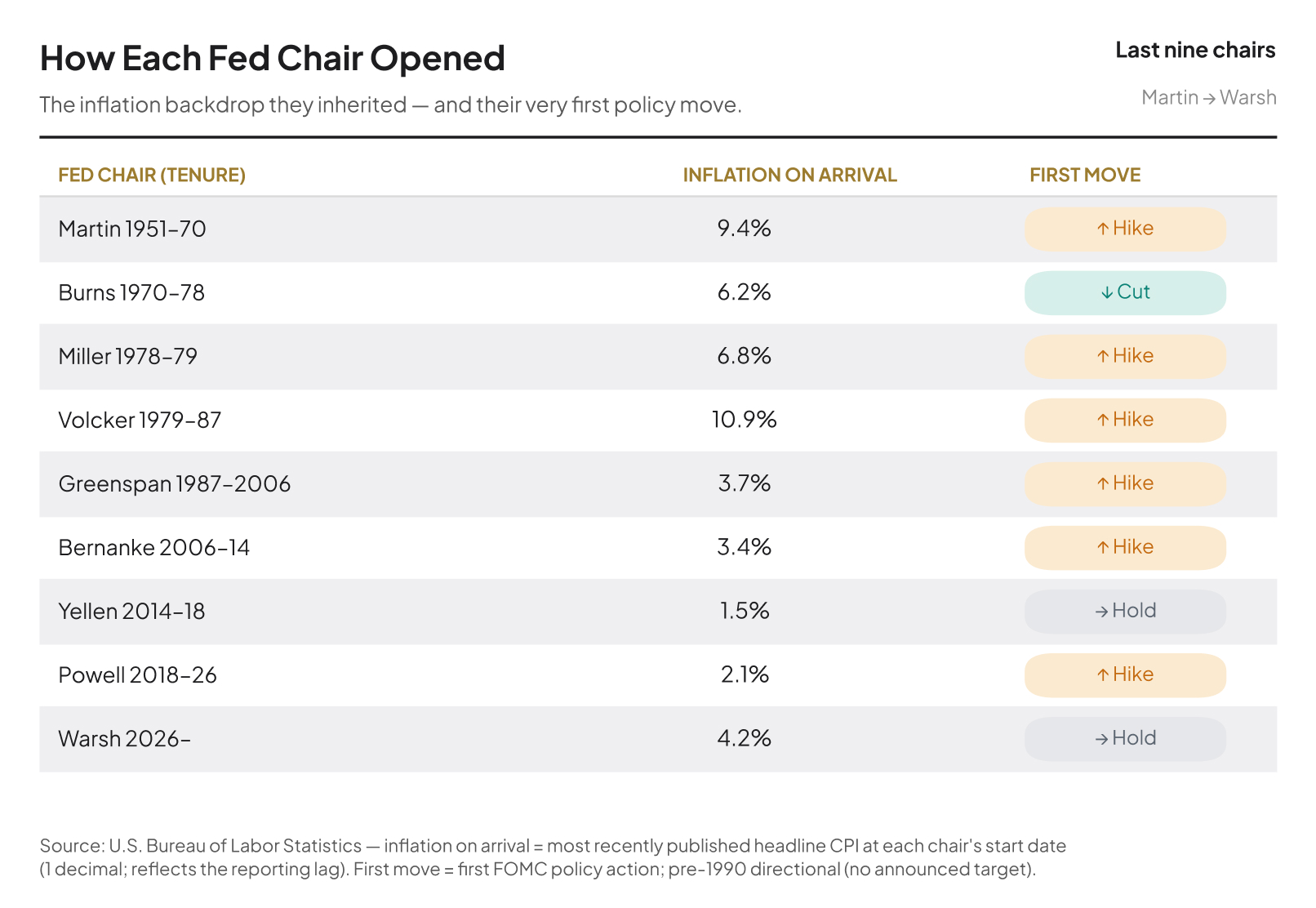

The hawkish debut itself is the least surprising part. New Fed chairs almost always come in sounding stern. But it's not about personality, it's the job. A brand-new chair has one thing to prove on day one: that they won't let inflation get away from them. The mandate is technically two jobs, full employment and price stability, but it's the price stability half where a new chair earns credibility. Until you've shown it, markets will test you, so you front-load the toughness.

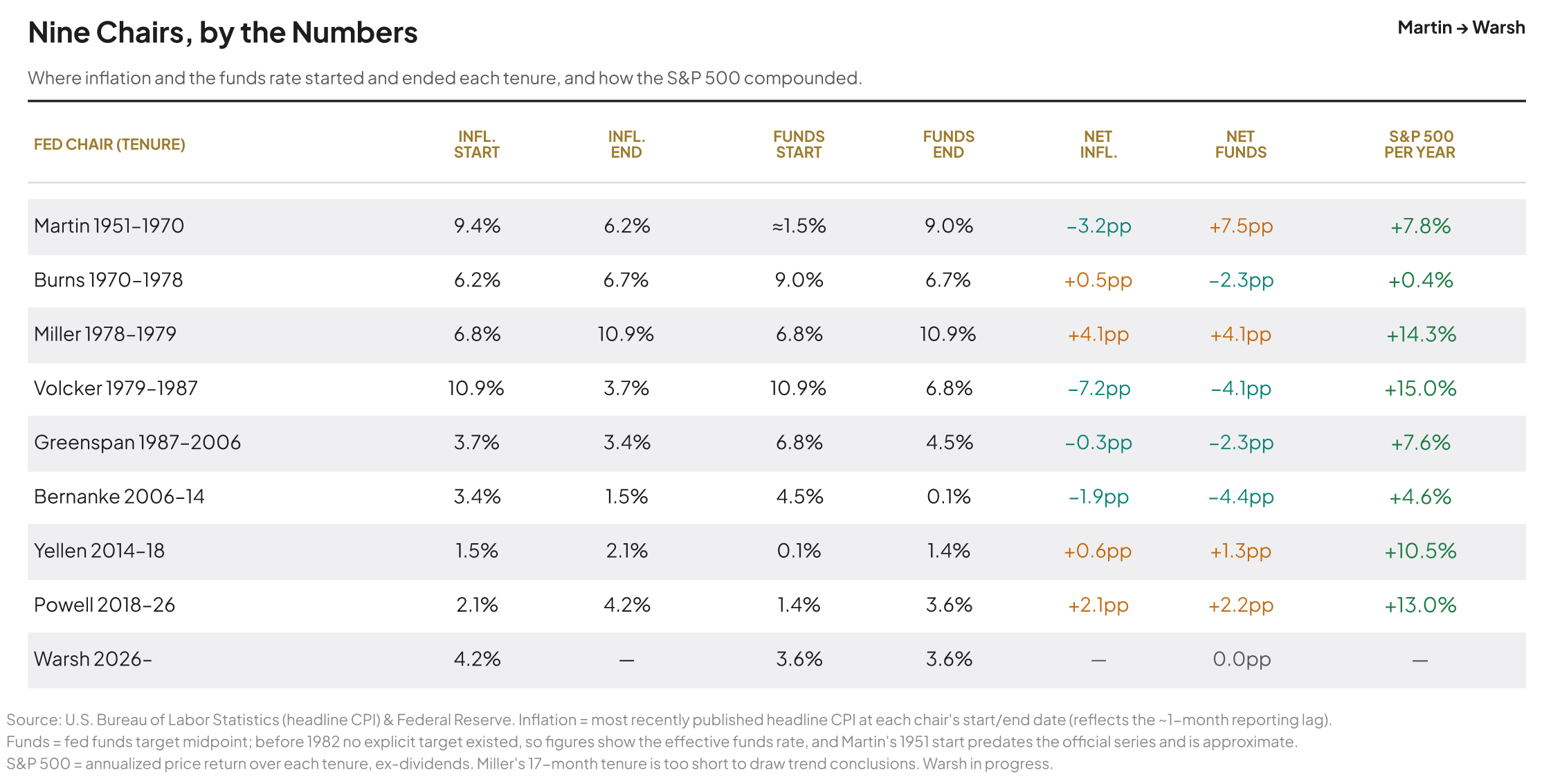

At his first meeting in 1979, Paul Volcker delivered a lecture on credibility while inflation was running north of 11%. Jerome Powell opened in 2018 by hiking and nudging up the projected path of rates. It isn't just those two. Of the eight chairs before Warsh, six opened by raising rates.

A firm tone is the standard, and Warsh faced an even higher hurdle than his predecessors, having been appointed by a President openly pushing for lower rates. Coming in soft would have looked like taking orders. Sounding tough on inflation was the only way to prove the Fed still answers to the data, not the White House.

The Fed used to be quiet

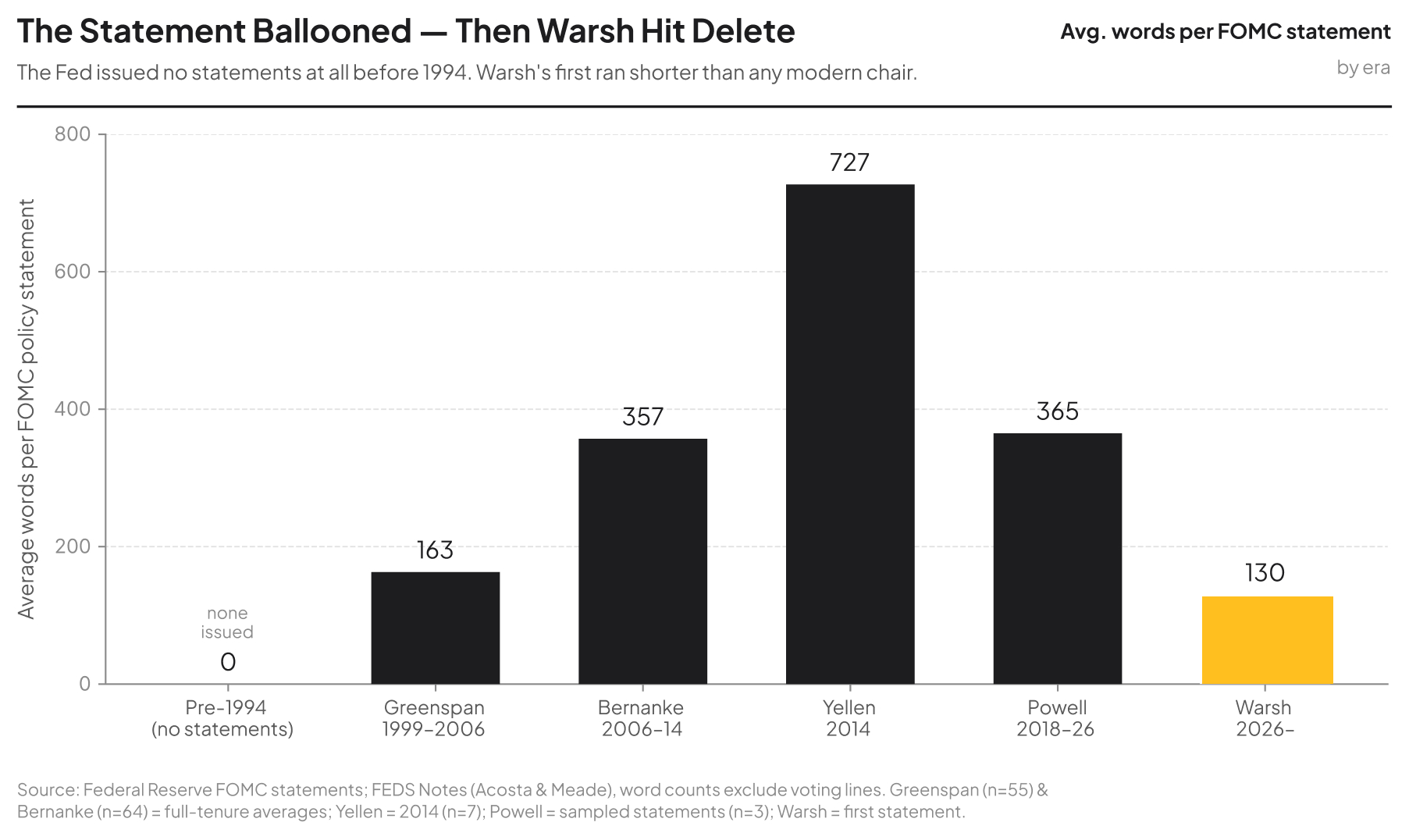

Warsh, wanting to say less than his transparency-dedicated predecessor, felt like an abrupt turn for a market that had grown accustomed to overdisclosure for the past decade or so. However, the chatty Fed is actually a fairly recent invention.

The first-ever post-meeting press conference didn't happen until 2011. The famous "dot plot" of rate projections only showed up in 2012. Before that, none of it existed. No pressers, no projection theater, no attempt to telegraph every move.

Go back a little further, and the Fed didn't even announce its rate decisions until 1994. Markets had to infer them by watching what the Fed did in the bond market.

The official Fed statement that is released before each press conference ballooned right along with the Fed's ambitions. Alan Greenspan’s statements ran a lean ~160 words on average; by the Yellen years, they'd swelled into 700+ word essays full of forward guidance.

While Powell began trimming them back, Warsh took an axe to the statement, with his very first clocking in at just 130 words. Barely a third of the 341 that the Fed had published one meeting earlier, and one of the shortest in the modern era.

So when Warsh signals he'll talk less and guide less, he isn't tearing up the rulebook. He's reaching back to an older one. For most of its history, the Fed was a tight-lipped institution that made its move and let everyone else do the interpreting.

The 1990s: A case study

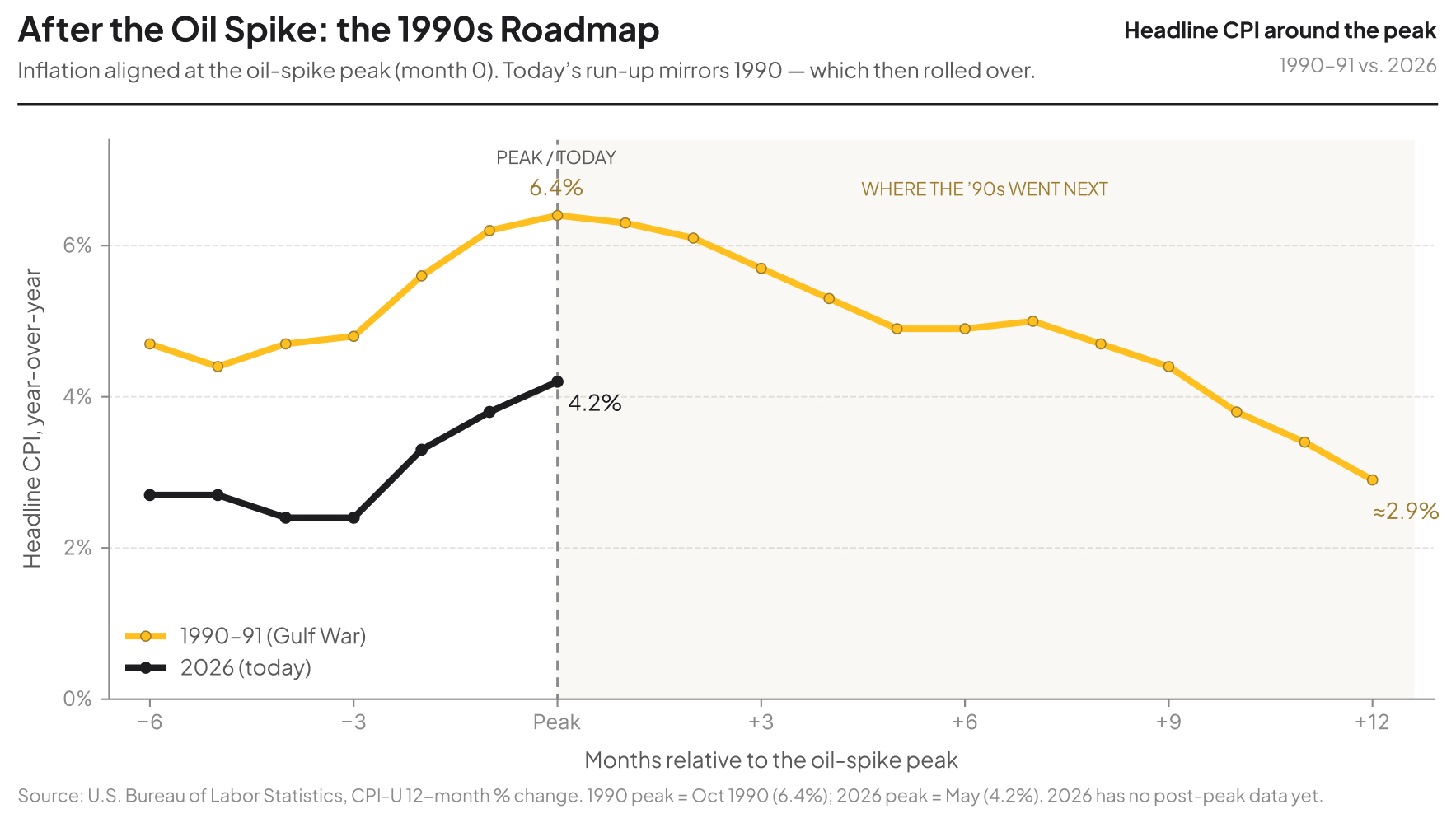

If this setup feels familiar, it should. We see parallels to the early-to-mid 1990s, a period deftly maneuvered by the legendary Alan Greenspan, who passed away just this week at age 100.

Back then, Greenspan faced very similar forces to those we face today.

- There was an oil-related inflation scare (the 1990 Gulf War spike, which pushed headline inflation to 6.4% even as underlying inflation stayed far calmer)

- We had a technology-driven productivity boom, driven by the internet, that quietly reshaped how hot the economy could run

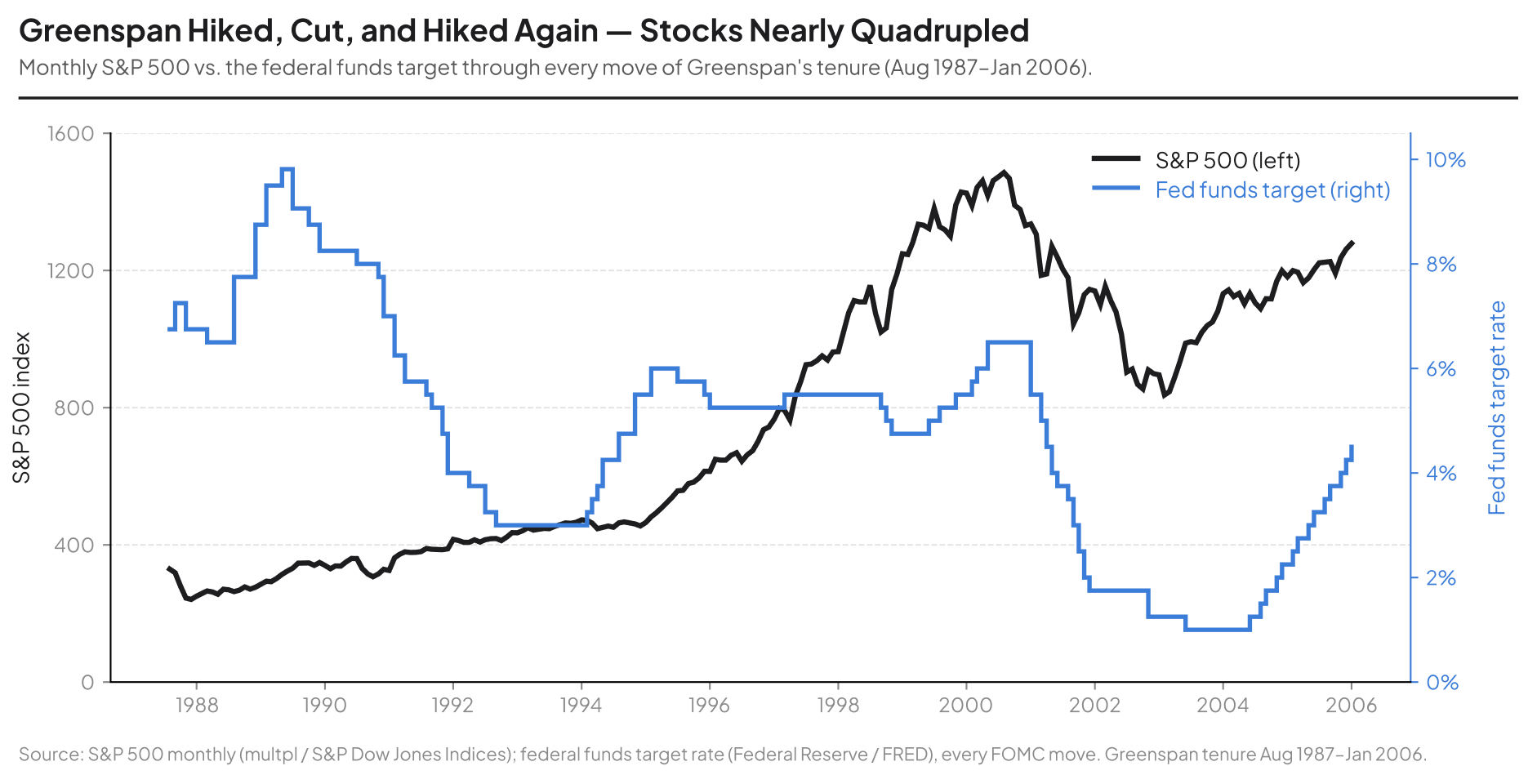

In response to this unique environment, Greenspan stayed nimble. He was unafraid to hike when it was warranted and cut when appropriate. The Fed funds target rate was far from a straight line or a clean story during his tenure. In fact, once the Fed began announcing its decisions in 1994, Greenspan changed the Fed’s target for the federal funds rate roughly once every three months, about four times a year. That is far more often than successors like Bernanke and Yellen, who left rates frozen for years at a stretch.

Along the way, he gave very little guidance to the market. Greenspan famously turned vagueness into an art form, once joking that if he'd made himself clear, you must have misunderstood him.

So how did the 90s ultimately turn out? By many conventional standards, pretty well. It’s a period remembered as a virtuous cycle of productivity gains and higher wages without higher consumer prices. The result was the rare combination of fast growth, full employment, rising real wages, and falling inflation at once.

That's the bull case for the Warsh era in a sentence: a quieter, firmer Fed that keeps its eye on the trend rather than the headline. One that sees the energy spike related to the Iran War already fading as the Strait of Hormuz reopens and crude rolls over, and also recognizes the productivity boon that could be on the horizon in the AI era.

Takeaways for investors

1. Markets need a Fed with credibility

At the end of the day, the central bank's most valuable asset is being believed. When markets stop trusting that the Fed is serious about inflation, the damage shows up fast and in places that matter. Long-term interest rates climb, rippling directly into mortgages, corporate borrowing, and the government's own interest bill.

The dollar tends to weaken, as global investors quietly trim their confidence in it as a store of value, while gold and other hard assets get bid up in its place. Most dangerous of all is what happens in people's heads: once households and businesses start to expect prices to keep rising with no reprieve, they act on it. Workers ask for bigger raises, companies push through pre-emptive price hikes, and inflation becomes self-fulfilling.

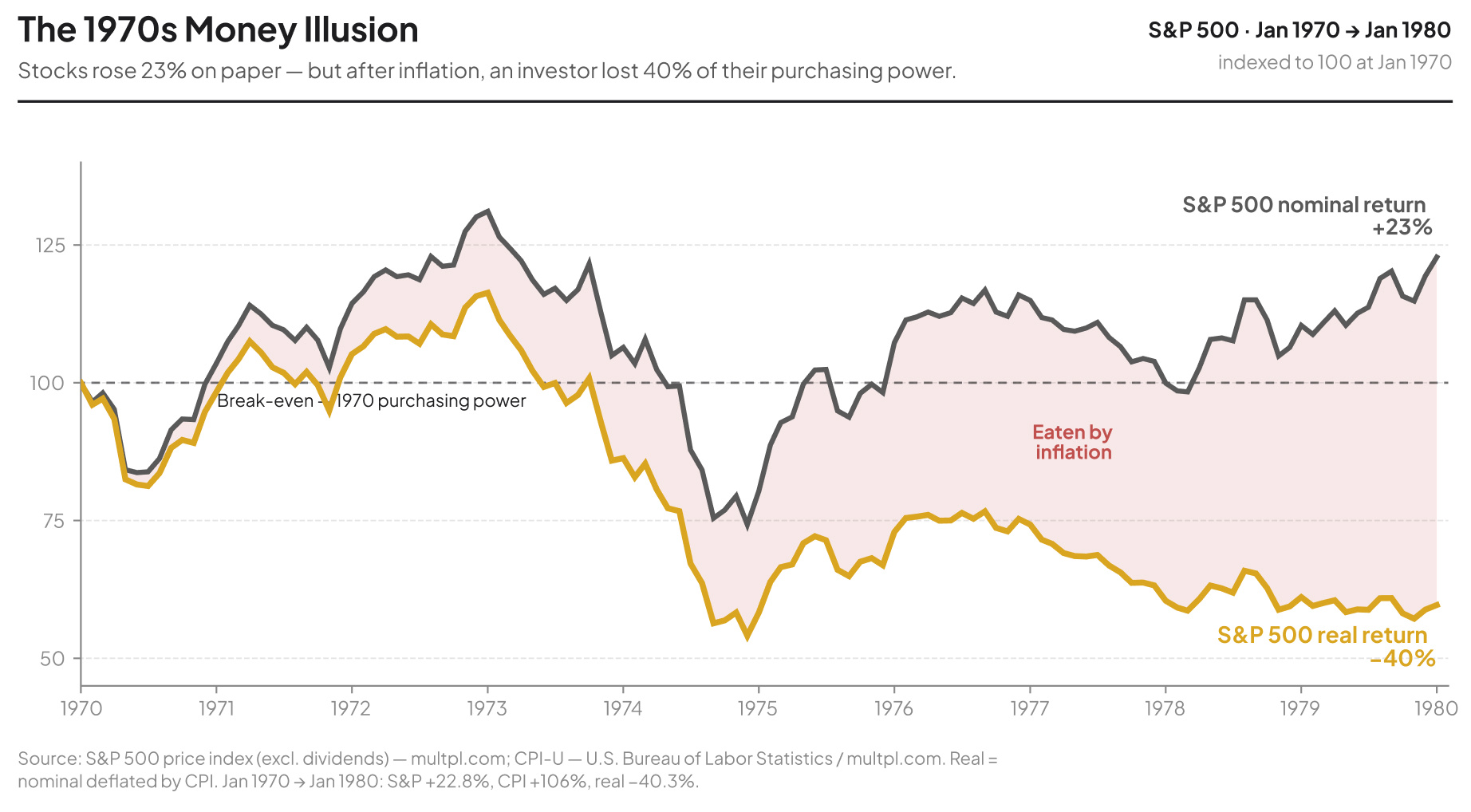

This played out in the 1970s. Inflation expectations came unanchored, a wage-price spiral set in, and headline CPI peaked above 11% in 1974 and again above 13% in 1980. The S&P 500 went nowhere for the entire decade. This is the spiral the Fed exists to prevent, and it's exactly why credibility, not any single rate decision, is the real prize.

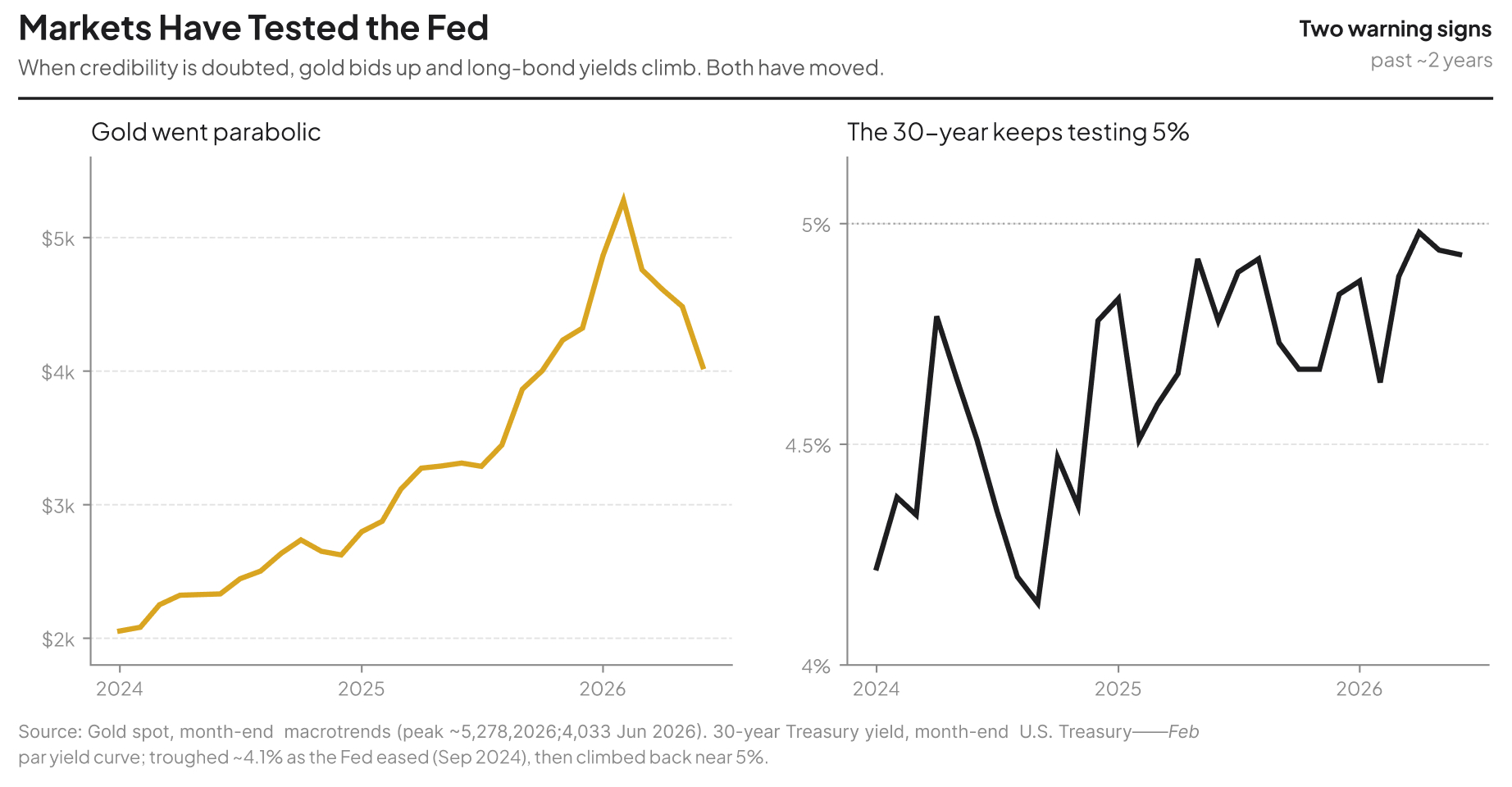

We’re not in the 1970s, but we've seen flickers of warning signs over the past year: gold surged to record highs, the dollar continued to slip versus other bellwether currencies, and long-dated Treasury yields have pushed higher.

There is no crisis yet. But it's the market's way of pricing a small, nagging doubt. Erasing that doubt is precisely the job Warsh was hired to do.

2. Less communication can lead to more effective monetary policy

Saying less can be a feature, not a bug. When the Fed narrates every move, markets stop analyzing the economy and start analyzing the Fed itself. It creates a meta-game in which markets start pricing in how they think the Fed will react to the data rather than the data itself. A quieter Fed can break that hall of mirrors. The Fed gets a cleaner read on how markets actually see the economy, while taking time to more quietly and deeply assess the data itself.

%201.jpg)

3. Short-term volatility may be the price of long-term stability

As the past week has shown, markets can be volatile when they are forced to digest higher-for-longer rates and fewer reassurances than investors have grown accustomed to. The S&P 500 is down ~2% since Warsh’s speech last Wednesday. But that discomfort is not necessarily bad news. A Fed willing to absorb short-term market pain in order to protect its credibility can create a more durable foundation for long-term investors.

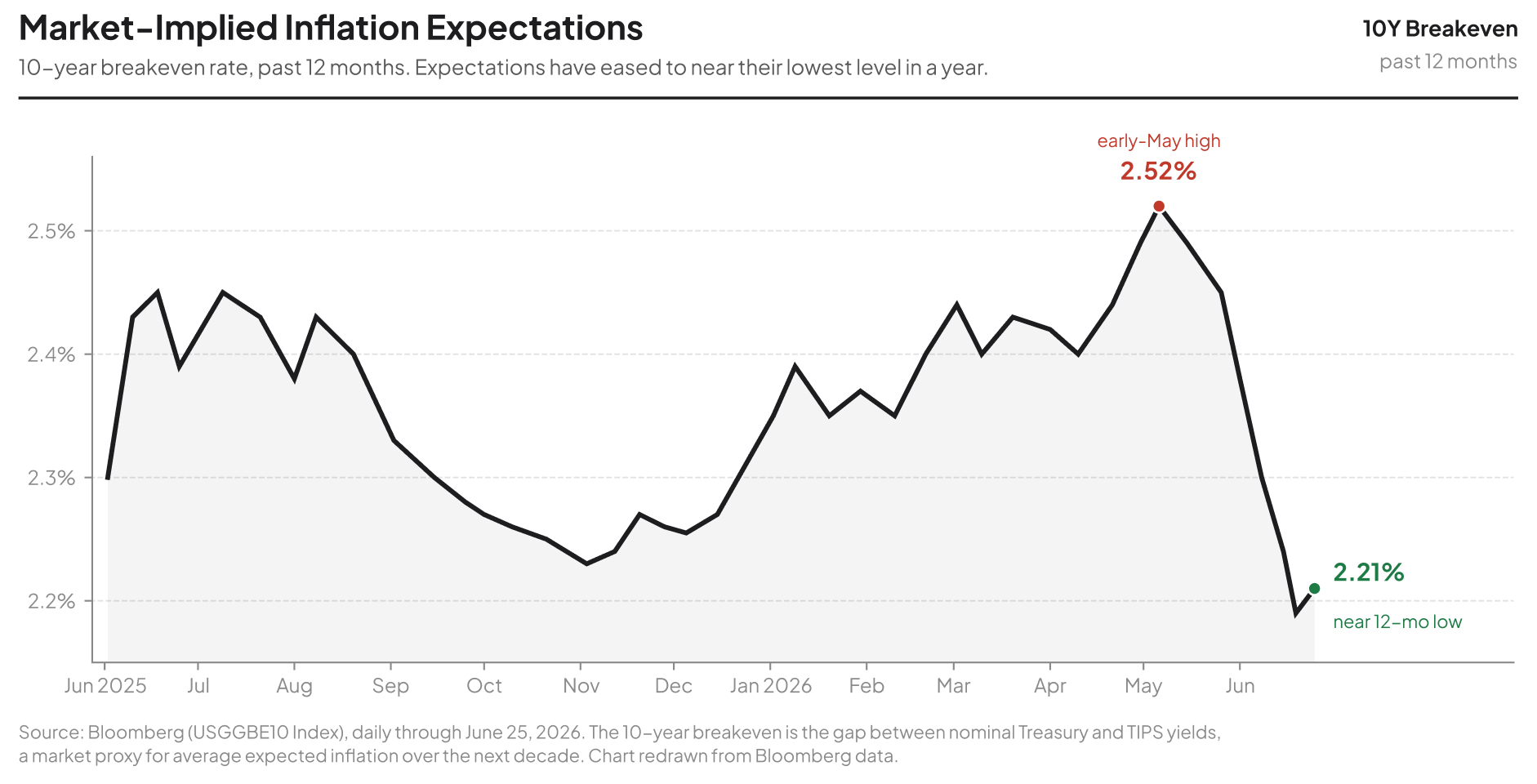

Early signs elsewhere in the market are encouraging. Since Warsh's nomination, the same indicators that had been flashing doubt about Fed credibility have started to turn. Gold has come off its highs, the dollar has firmed, and long-term yields have eased. Perhaps most notably, market-implied inflation expectations have continued to move down and are now at 12-month lows. Those are the first places confidence tends to show up when investors believe the Fed means what it says.

The longer historical record is more reassuring still. Stocks have performed well under very different Fed regimes. The S&P 500 nearly quadrupled under Greenspan, but it also compounded at healthy rates under the notoriously hawkish Volcker and the notably dovish Yellen. The chair’s name, style, and temperament have mattered far less to long-run returns than whether the institution stayed credible, inflation expectations remained anchored, and policy kept responding to the data.

That is the constructive case for investors. A quieter and firmer Fed may create more day-to-day uncertainty, but it can also reduce the larger risk: a central bank that markets stop believing.

Disclaimer: The information contained in this communication is for informational purposes only. This content may not be relied on in any manner as legal, tax, regulatory, or investment advice. Range Advisory, LLC and Range Tax, LLC are wholly owned subsidiaries of Range Finance, Inc (“Range”). Tax services are provided by Range Tax, LLC. Investment advisory services are provided by Range Advisory, LLC. Range Advisory, LLC is an SEC-registered investment adviser. Registration with the SEC does not imply a certain level of skill or training. Range Advisory, LLC does not make any representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein and nothing contained herein should be relied upon as a promise or representation as to past or future events. All investments involve a high degree of risk, including the possible loss of some or all of an investment. Range Advisory, LLC pricing and additional information can be found at www.range.com.

.svg)

.svg)

.svg)