Oil and Recessions

It's been well documented that geopolitical shocks rarely have lasting economic consequences. Looking back at major events since World War II, markets have typically dipped around 5% before bouncing back in under three weeks.

So why does oil get so much attention?

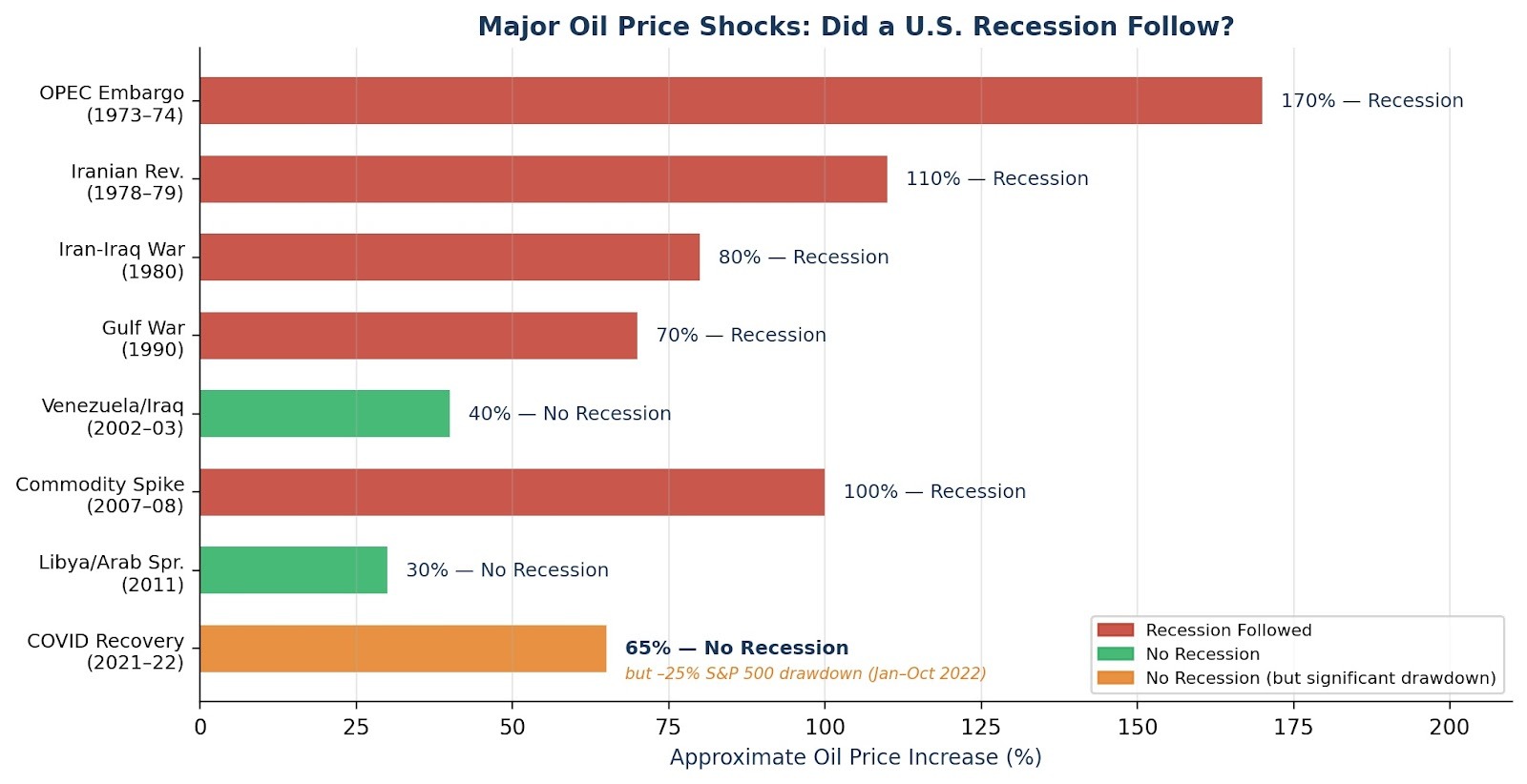

Because the exceptions—the shocks that do cause lasting damage—often share a common thread: they come with a meaningful, sustained rise in oil prices. Economist James Hamilton's landmark 2011 study found that all but one of the 11 post-WWII U.S. recessions were preceded by a significant increase in oil prices.

But the reverse is not a hard-and-fast rule: an oil shock does not guarantee a recession. To separate a temporary market scare from a material economic catalyst, we have to look more closely at the underlying environment.

What Makes the Exceptions

Research shows that for an oil shock to produce a meaningful 15%+ drawdown in equity markets, at least one of the following conditions must be met:

- The spike is large and sustained — An oil price increase of 50–100%+ that persists over several months, long enough to embed itself in consumer and corporate behavior

- Existing economic vulnerability — A shock to an already-slowing economy can quickly tip it into recession

- A hawkish Fed response — If the shock forces central banks to fight the resulting inflation with aggressive rate hikes, economic growth can be choked in the process

Right now, we're not clearly meeting any of these criteria—but this is a dynamic situation. Here's where things stand:

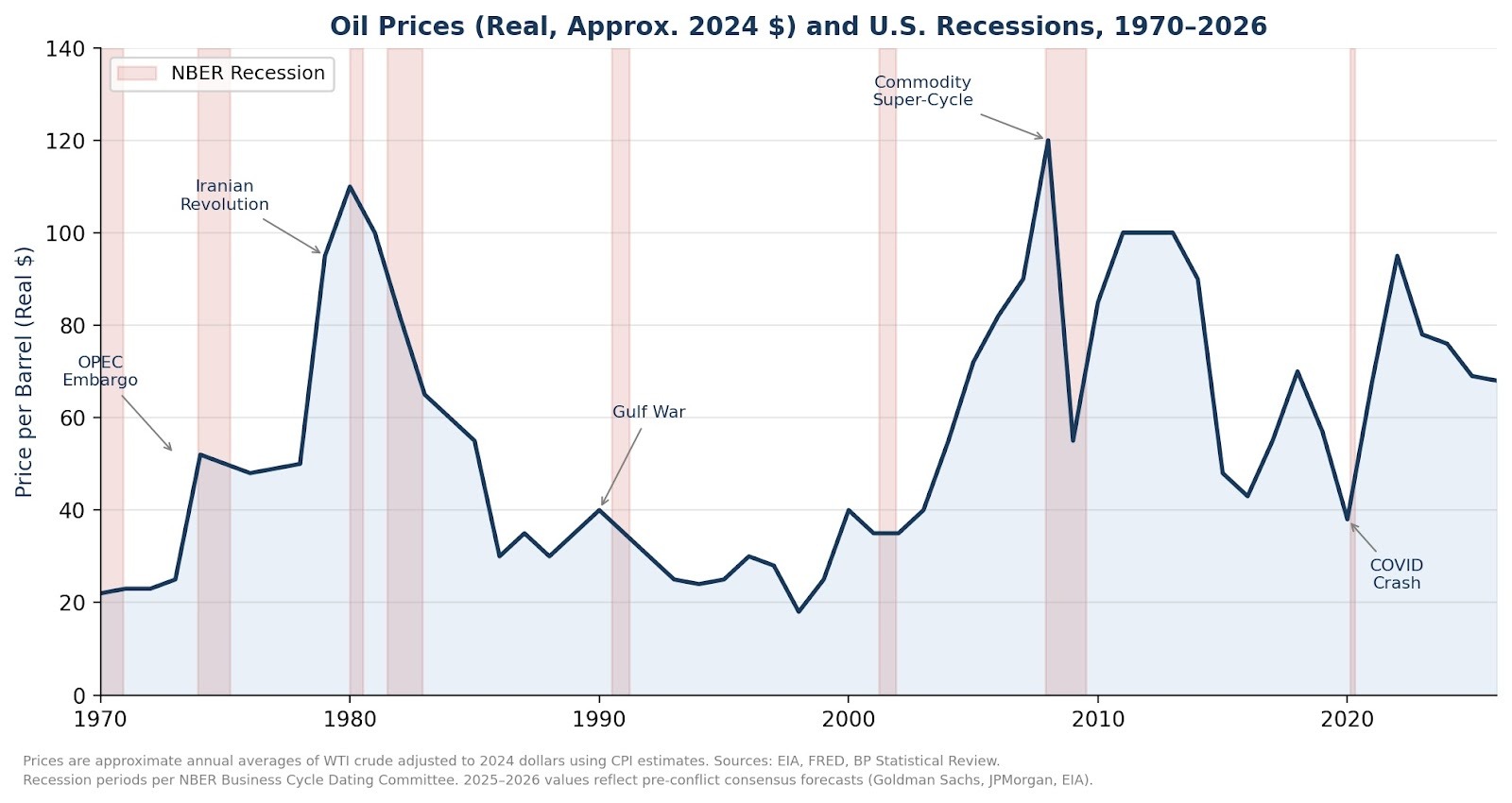

Criterion 1: Severe, Sustained Oil Shock

Nearly every recession-linked shock involved an oil price spike of at least 70%. During the OPEC embargo, the Iranian Revolution, and the 2007–08 commodity super-cycle, prices spiked well past that threshold and stayed elevated long enough to fundamentally alter business and household spending.

Conversely, smaller spikes with quicker reversals have typically been absorbed. The supply disruptions from Venezuela in 2002 and the Arab Spring in 2011 saw price increases of 40% and 30% respectively yet economic expansion continued.

So where are we now? Goldman Sachs estimates the "unaffected" price of Brent—which strips out the Iran conflict risk premium—is approximately $66 per barrel. As of Friday's close, Brent settled at $92, nearly 40% above that baseline.

This premium is driven almost entirely by uncertainty around the Strait of Hormuz, a critical chokepoint responsible for roughly 20% of global oil supply. Iran controls the northern side, and tanker traffic has collapsed from an average of 24 vessels per day to near zero since the strikes began.

How high oil goes from here depends almost entirely on the duration of the disruption. Analysts estimate a war lasting more than three weeks could push Brent above $100. JPMorgan has warned that if storage capacity in Gulf countries becomes exhausted, prices could reach $120. A Deutsche Bank strategist noted this week that under extreme scenarios involving a full closure, $200 isn't off the table.

This week's roughly 35% surge in crude oil was the largest since at least 1985. While near-term prices are impossible to predict, a continued climb at this pace would steadily raise recession odds. Rapidan Energy's Bob McNally, a former White House energy advisor, put it bluntly: "A prolonged closure of the Strait of Hormuz is a guaranteed global recession."

We're not there yet, but the market's buffer is getting thinner.

Criterion 2: Already-Slowing Economy

History shows that oil shocks can cause more damage when they hit an economy that's already losing momentum. In 1973, the OPEC embargo landed on an economy already contending with building stagflation. The 1990 Gulf War shock struck at the tail end of a mature business cycle that was already rolling over. And in 2007–08, the commodity super-cycle unfolded alongside a crashing housing market and a credit system under severe stress. In each case, the oil shock amplified economic weakness that was already there.

Today's economy looks softer than it did a few months ago, but it isn't raising red flags.

Labor market: Friday's jobs report indicated that unemployment ticked up to 4.4% in February as payrolls fell 92,000—the third decline in five months. Much of the weakness has identifiable, temporary drivers: a Kaiser Permanente strike that sidelined 28,000+ healthcare workers and weather-related pullbacks in construction. Overall, unemployment remains below its long-run historical average, and the rise from the 2023 low has been a gradual drift, not the sharp spike that has accompanied historical downturns.

Corporate earnings: S&P 500 companies just wrapped up a Q4 2025 earnings season that surprised to the upside—14.2% year-over-year earnings growth, the fifth consecutive quarter of double-digit expansion. Analysts are still penciling in a healthy 15%+ growth for the rest of 2026.

GDP: Q4 2025 came in at 1.4% annualized—soft on the surface, but largely explained by the federal government shutdown. For Q1 2026, the Atlanta Fed's GDPNow model estimates GDP growth of 2.1%.

Overall, the economic picture is mixed—there are signs of modest softening, but we're not seeing the broad-based deterioration that has historically turned an oil shock into a recession.

Criterion 3: Hawkish Fed Response

When oil prices spike, central banks often have to raise rates to fight the resulting inflation, making an already-difficult environment even harder for businesses and consumers to navigate.

The Iranian Revolution unfolded just as former Fed Chair Paul Volcker was beginning his historic fight against inflation. During the Iran-Iraq War, the Fed pushed rates to 19% in the ten months between the oil shock and the recession that followed. In 2022, oil spiked into an already-hot inflation backdrop, forcing the most aggressive rate-hiking campaign in four decades, which contributed to a 25% drawdown in the S&P 500.

Today is different. The Fed has already cut rates six times since September 2024 and markets still expect the Fed to be on an easing path.

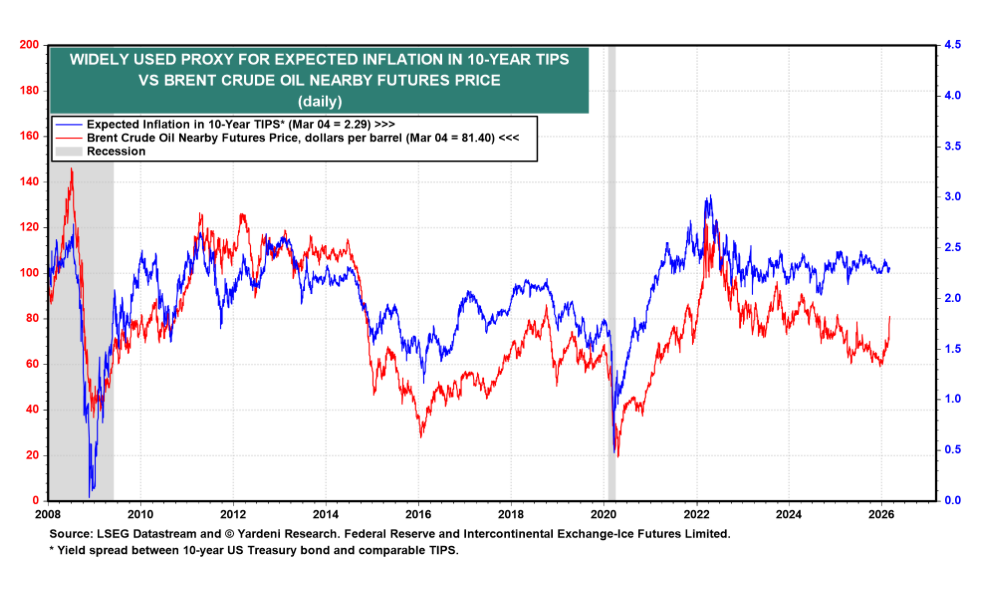

The Fed has room to keep cutting because inflation expectations remain anchored. Yardeni's chart below shows that long-term inflation expectations (as measured by the 10-year TIPS breakeven) have historically tracked oil prices closely. Right now, while crude has spiked sharply, inflation expectations have barely moved. Markets don't yet believe this shock will reignite durable inflation.

That could change. If Brent stays elevated, inflation expectations are likely to move higher, causing the Fed to lose flexibility. A boxed-in Fed—one that can't cut even as growth slows—is a dangerous regime for markets.

We're already seeing signs of that pressure building in Europe. Eurozone inflation surprised to the upside in February. More recently, European natural gas prices have surged nearly 74% since the strikes began, driven by the disruption to LNG flows through the Strait. As a result, the market has gone from anticipating multiple rate cuts by the ECB this year to pricing them out almost entirely, posing a meaningful headwind for the region.

The Bottom Line

As of this writing, the current move in oil, while significant, remains well below the sustained, structural spikes that preceded the worst historical downturns. The U.S. economy is still growing, and the Fed is still focused on easing.

If oil prices stabilize and this combination holds, the episode may well look more like 2002 or 2011—disruptive, yet ultimately absorbed.

But as the military strategist Carl von Clausewitz famously noted, war is "the realm of uncertainty." We may not be in recession territory yet, but as long as this conflict continues, our economic margin of safety is shrinking.

Disclosure:

This communication is for informational purposes only and does not constitute investment advice or a recommendation to buy, hold, or sell any security. Forward-looking statements involve risks and uncertainties. Past performance is not indicative of future results.

.svg)

.svg)

.svg)