At the start of 2026, we published a market outlook built on a clear set of assumptions: inflation cooling, the Fed continuing to ease, and a long-awaited rotation away from mega-cap tech. For a while, that's exactly what happened. Then an escalation of the conflict in Iran changed everything.

We sat down with our Chief Investment Officer, Taresh Batra, to make sense of it all: what we got right, what surprised us and how to think about positioning for the rest of the year. Here's that conversation.

Q: Q1 is in the books — how has the year unfolded so far relative to your expectations?

There are some things we got really right… and some things that surprised us.

One thing we got right was the rotation away from large-cap US stocks. We said small and mid-cap stocks offered better upside relative to large-caps, that international stocks were poised to continue performing well, and that investors who were overconcentrated in US mega-cap tech were taking on more risk than they realized. All of that played out.

At the start of the year, we espected 2026 would benefit from policy clarity and stability. Tariff uncertainty was behind us, tax policy was settled, and most importantly, we had consensus around a Fed that would continue easing monetary policy in 2026.

But the war in Iran shattered any illusions of macro stability. Just like much of last year, we are back in an environment where policy headlines are driving markets and fundamentals have taken a back seat.

Q: Let's start with what you got right. You expected a rotation away from big tech into small and mid-cap stocks and international stocks. How has that played out?

Our view at the beginning of the year was that small and mid-cap stocks offered asymmetric upside relative to their large-cap counterparts. These companies had already absorbed the worst of the Fed's rate-hiking cycle, and their earnings were just beginning to recover. They were also significantly cheaper than large-caps, setting up a potential double-tailwind: accelerating earnings and expanding multiples.

We also wrote that international stocks were positioned to continue performing well. Europe, in particular, had powerful fiscal tailwinds alongside an accommodative ECB (European Central Bank). International stocks also had cheaper valuations and significantly less exposure to "bubble" risk in U.S. mega-cap tech.

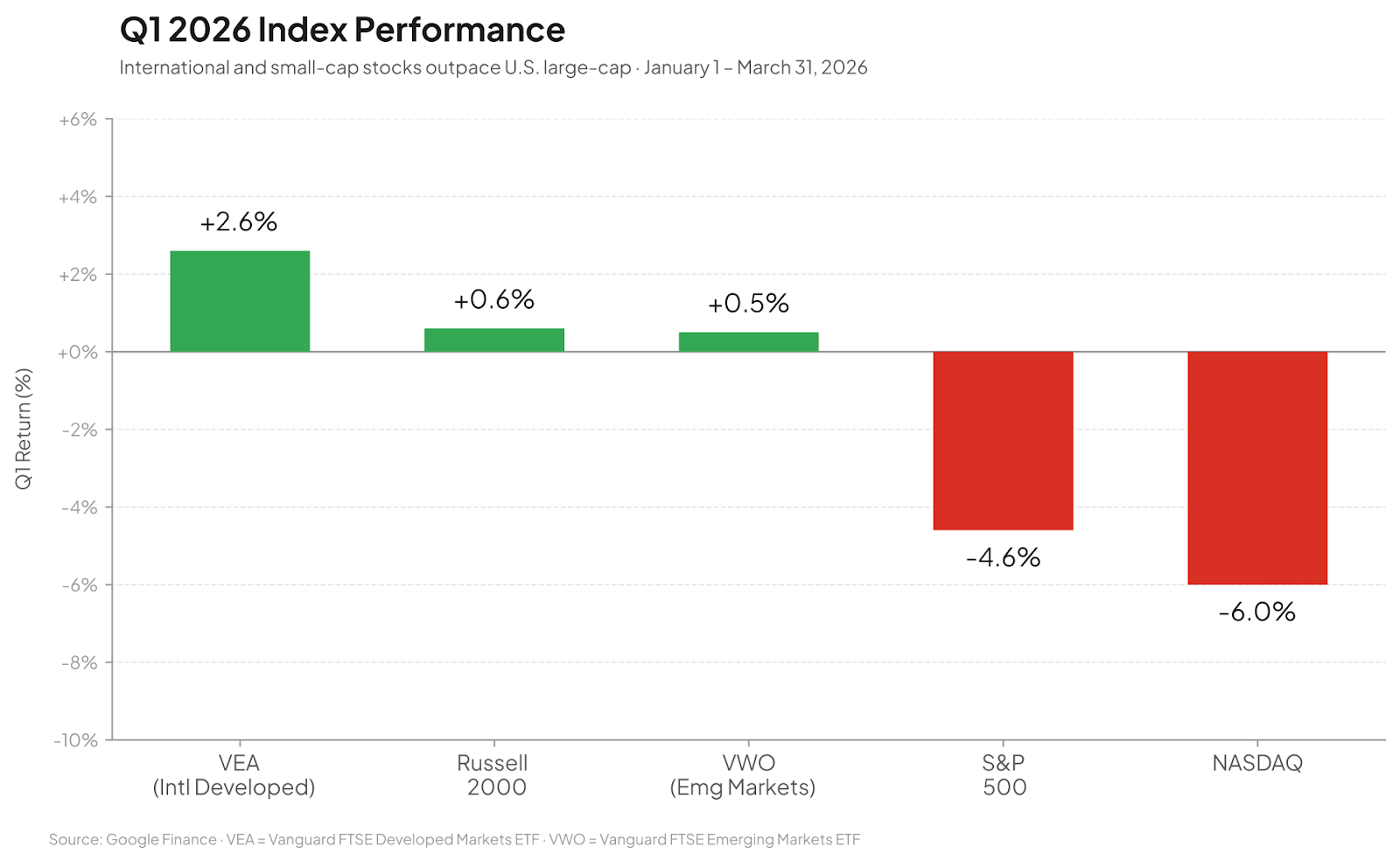

For the first two months of the year, the rotation played out pretty much as forecast. Through the end of February, the small and mid-cap heavy Russell 2000 was already up roughly 6% while the S&P 500 was essentially flat. International stocks got off to a blistering start, with international indices posting double-digit gains in just eight weeks.

The war in Iran derailed this momentum — but overall, diversification still paid off meaningfully in Q1. The S&P 500 ended the quarter down roughly 4.5% while small and mid-cap stocks and major international indices ended the quarter in the green.

If you had a properly diversified portfolio, you navigated an incredibly volatile period with minimal damage. If you were overconcentrated in tech, last quarter was a painful wake-up call.

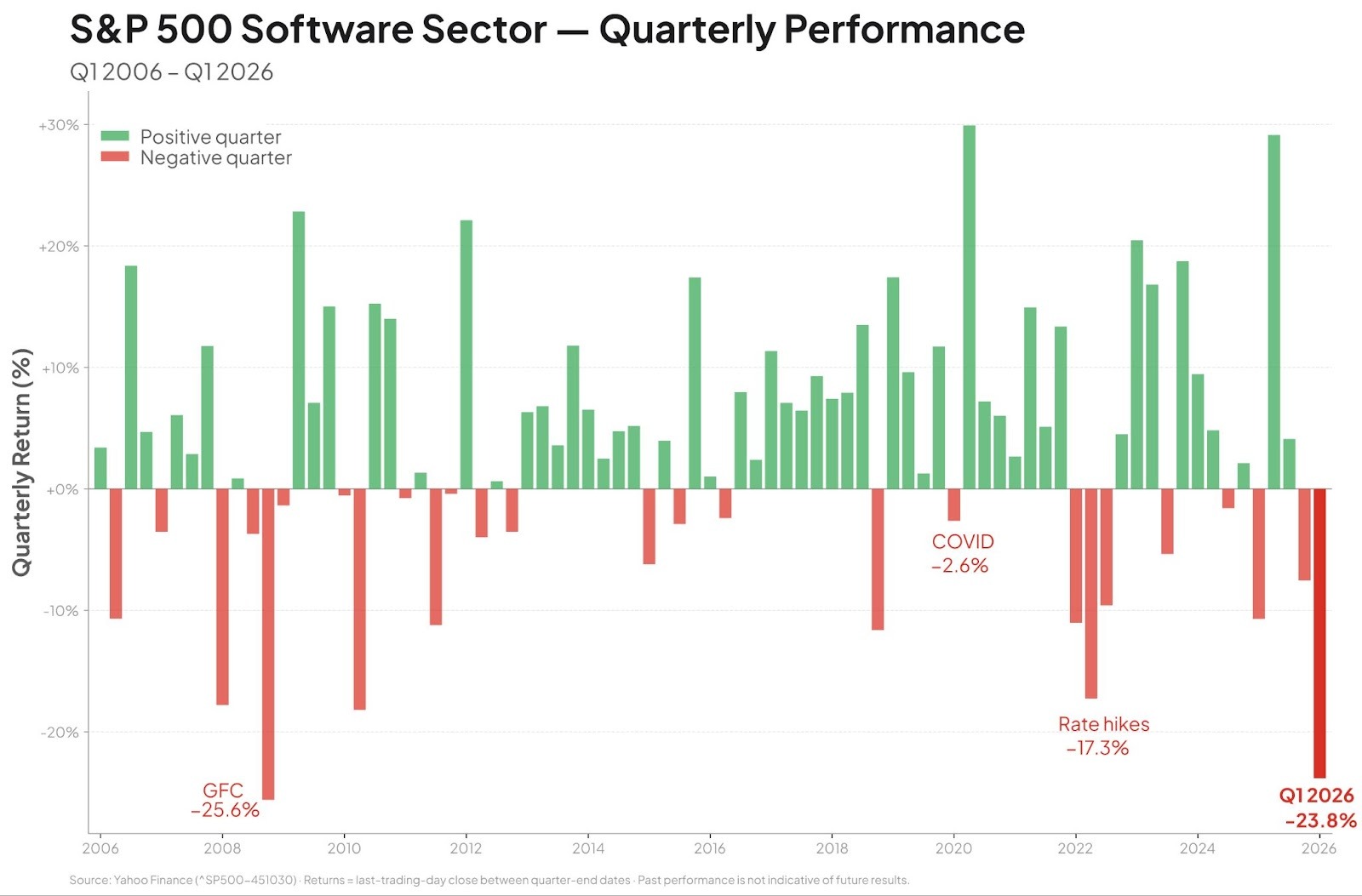

Q: Speaking of tech — software got hammered in Q1. Did you see that coming?

We cautioned against going "all-in" on tech, but we certainly didn't anticipate the severity and speed of the drawdown. The software sector fell 24% in Q1 — its worst quarter since 2008. The Nasdaq fell nearly 6%, its worst quarter since 2022. That said, we know that violent sector moves like this are nearly impossible to predict, which is exactly why diversification matters.

What we did say at the beginning of the year is that we were deeply concerned about private markets and viewed them as especially vulnerable to AI-related risks. That vulnerability got exposed even faster than we expected.

Private credit and private equity have outsized exposure to the software sector. As investors realized the real threat AI poses to many of these funds’ portfolio companies, the sentiment shift around these asset classes was swift.

Blue Owl, a heavyweight in tech lending, faced a 'bank run' as investors requested to pull 40.7% of the total capital from its flagship technology fund in Q1 alone. To prevent a total collapse, the firm was forced to 'gate' the fund, leaving billions of dollars in redemption requests effectively trapped. Other industry titans like Apollo and Ares were also forced to hit the emergency brakes and cap redemptions.

For some of these software companies and private credit firms, the sell-off is likely overdone; but it’s clear the 'bulletproof' perception of these sectors has been shattered.

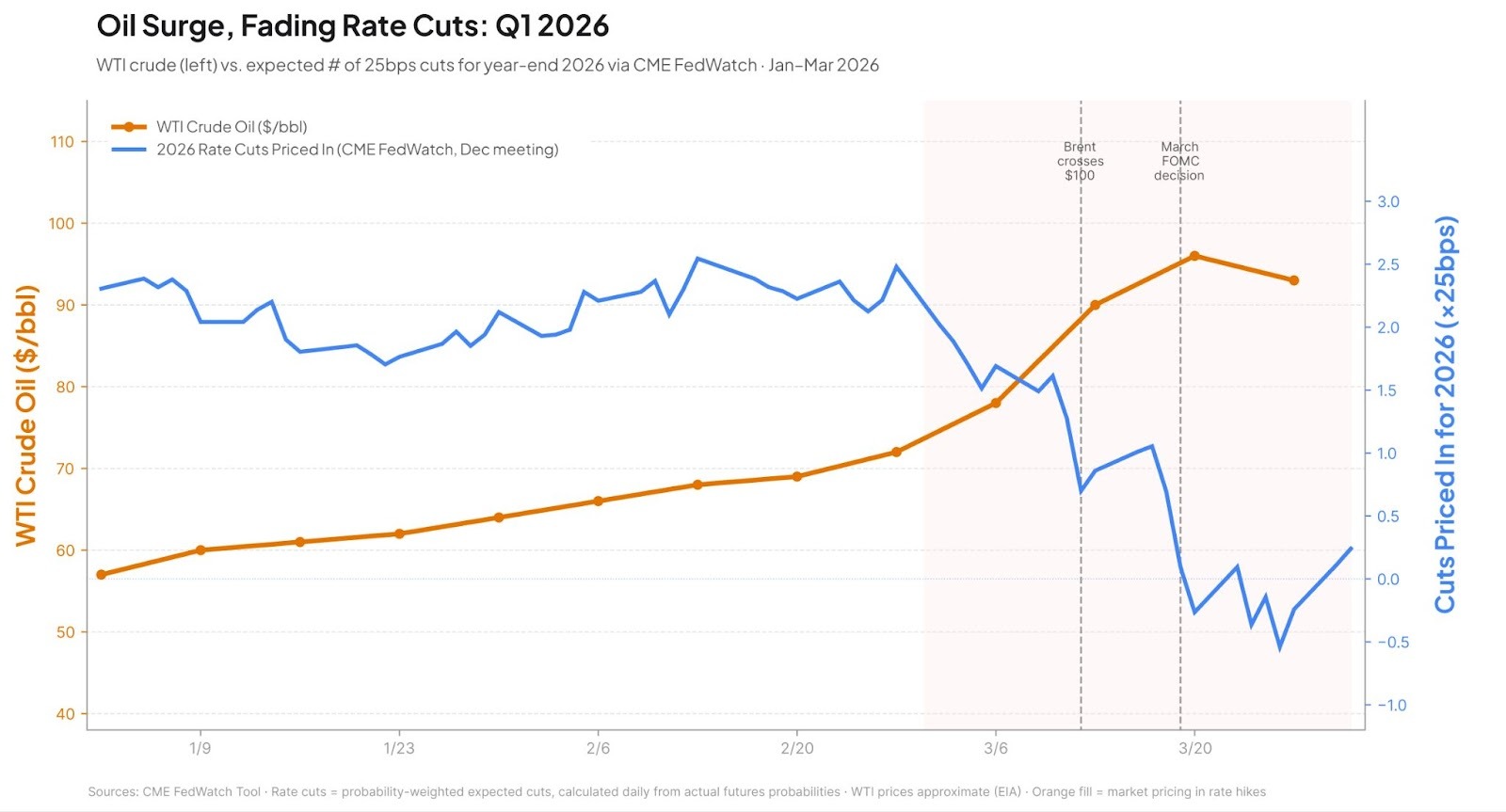

Q: The macro stability you expected hasn't materialized. Is the rate-cut thesis dead?

It's hard to believe, but for the fifth year in a row, we're once again talking about "transitory" inflation.

Coming into the year, our view was that inflation was decelerating and the Fed was stepping up to support the economy — not only through rate cuts but also by providing liquidity through the balance sheet.

With Brent crude surging nearly 60% from around $60 per barrel at the start of the year to nearly $100 today, there's a lot less clarity on the path of inflation and, by extension, monetary policy.

In turn, the market has almost completely erased expectations of rate cuts this year and even briefly priced in a greater than 50% probability of a rate hike by year-end.

We don't share that view. We still think the Fed cuts this year.

Start with inflation itself. Like the inflation spikes driven by COVID and tariffs, this looks more like a temporary supply shock than a structural change in the inflation picture. Oil prices are well above levels justified by fundamental demand, and we may be at or near peak supply disruption. If so, energy prices should move lower from here.

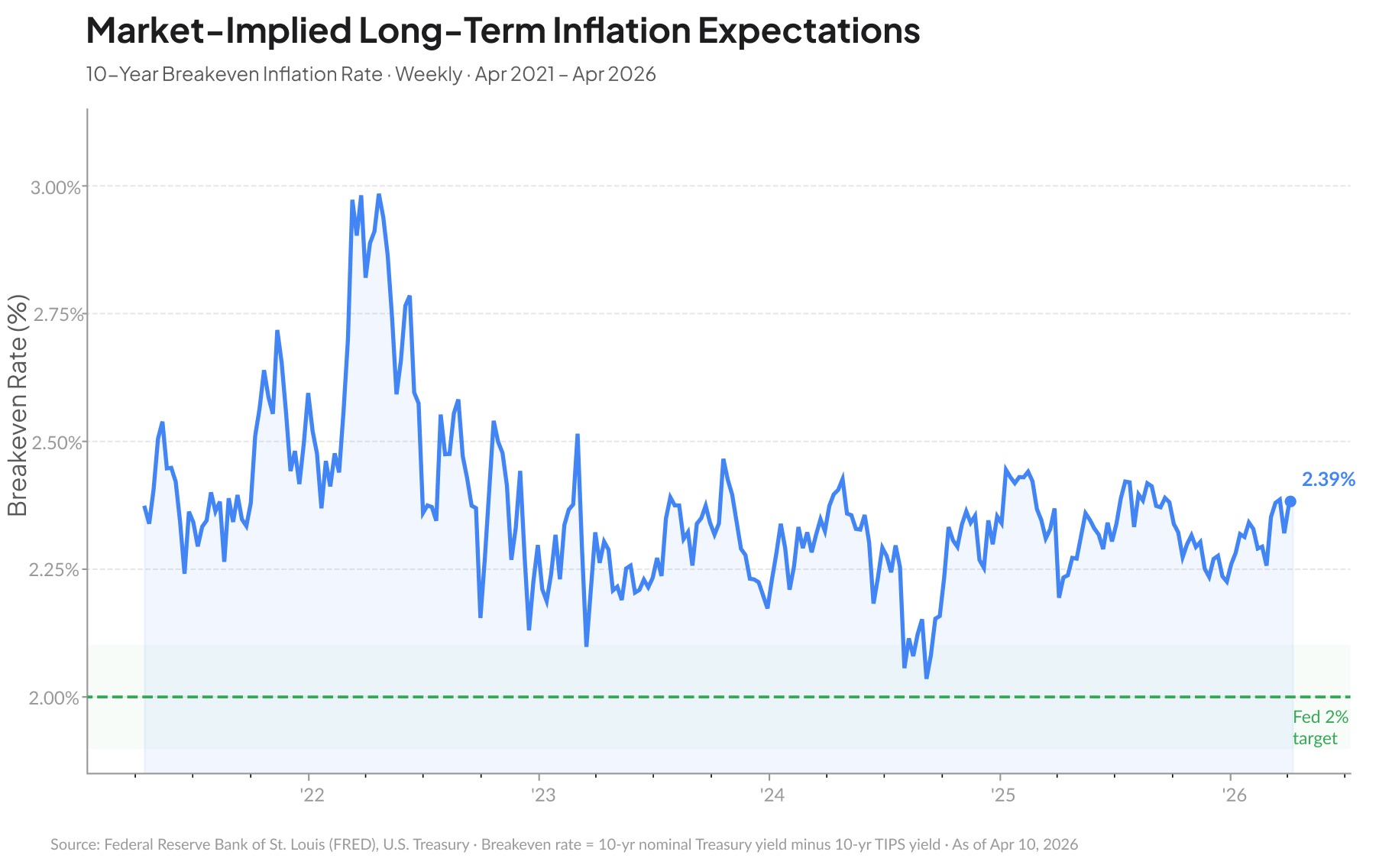

It’s also important to note that while the energy-related price spike will show up in headline inflation, the Fed pays much closer attention to core inflation, which strips out energy. It’s possible the energy shock begins to bleed into broader prices, but we’re not there yet. The March CPI report released today showed headline inflation accelerating but core inflation actually coming in cooler than forecast, rising only 0.2% m/m.

A deeper look into market indicators supports this view. Long-term inflation expectations are currently at 2.39%, having barely budged since the beginning of the year.

Most importantly, we know the Fed has a dual mandate. They don't just manage inflation — they also seek to maximize employment. Higher oil prices are already squeezing consumers and corporations, reducing demand and slowing growth. A rate hike would compound that pressure: tighter financial conditions mean a harder environment for businesses, more pressure on employment, lower brokerage and 401(k) balances, and weaker consumer spending.

We don’t think the Fed opts to tighten the screws further. A 'hold' may be the baseline, but we think the market is underestimating the odds of a cut—whether it’s driven by a return to disinflation as this conflict de-escalates or simply as insurance against a hard landing.

Q: So what does this ultimately mean for markets? How should investors be positioned?

We’re still constructive. There's no doubt the outlook has gotten murkier, but the underlying fundamentals haven't cracked.

The macro data is holding firm. We added 178,000 jobs in March and industrial production has been positive for several months now after a long period of declines. On the earnings side, estimates for 2026 are actually moving higher, not lower — S&P 500 companies are now expected to grow earnings by 17% this year, up from the 12% expected back in January. Credit markets are also showing resilience. Credit spreads have widened modestly from their January lows but remain a far cry from levels usually seen in a recession.

All of this tells us the U.S. economy is still operating from a position of strength. The longer oil prices stay elevated, the more that strength gets tested, but there is runway to absorb temporary headwinds.

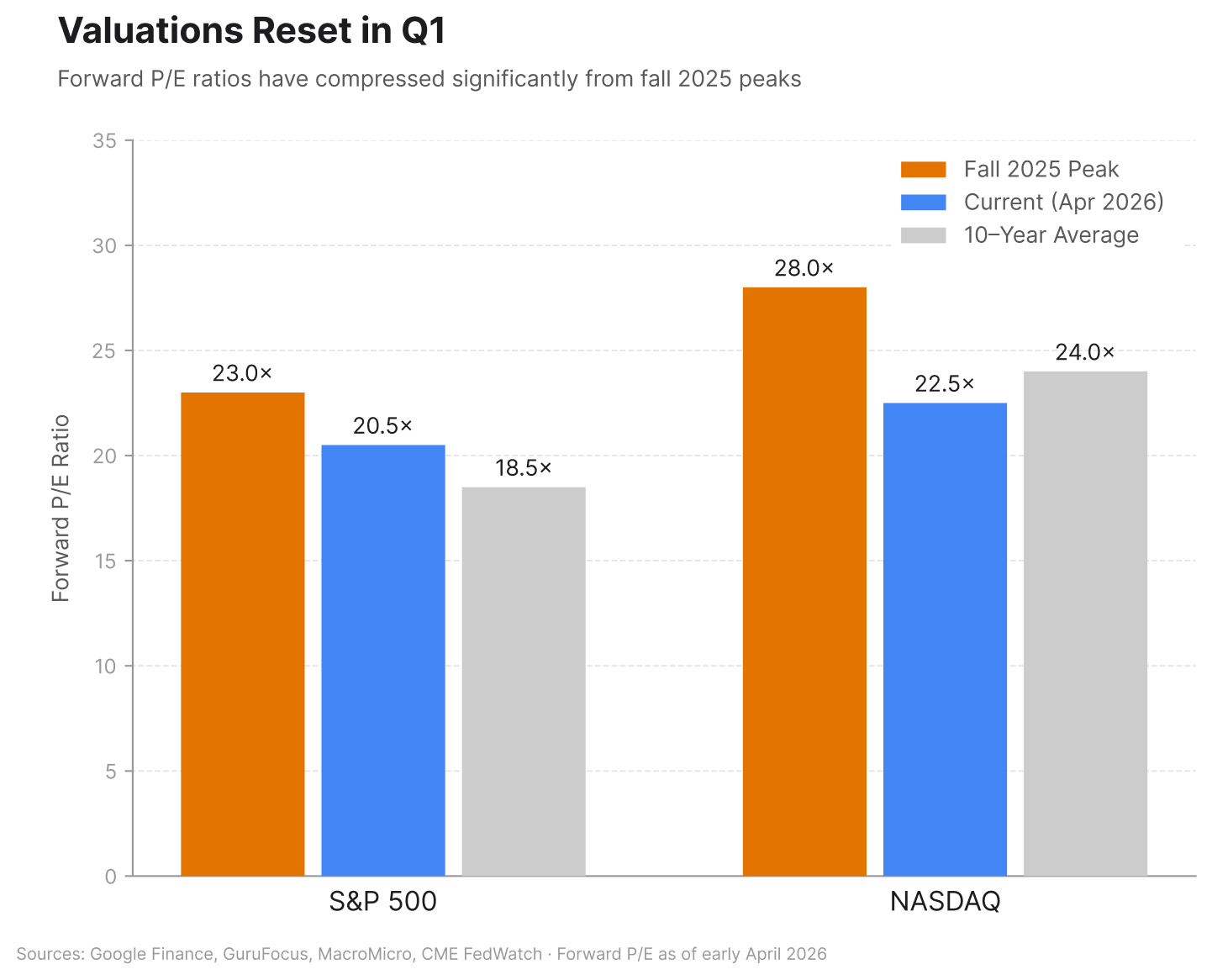

Valuations, meanwhile, have already reset lower. The S&P 500's forward P/E, the price investors are paying for future earnings, has declined to roughly 20x from 23x last fall. The compression in the tech sector has been even more pronounced. The tech-heavy Nasdaq index is now trading at 23x forward P/E, down roughly 20% from last fall’s peak and now below the 10-year average of nearly 24x. In terms of valuation, we have a much better entry point for equities today than we did in January.

We expect diversification to continue to pay off. If Q1 taught us anything, it's that the concentrated mega-cap trade that dominated the last two years can no longer be taken for granted. International equities arguably have the most to gain from the de-escalation of the Iran conflict and a decline in energy prices. Domestically, small and mid-cap stocks will benefit most if the Fed returns to monetary easing.

That being said, it’s important not to move too far away from large-caps, which look more attractive today than they did at the beginning of the year. If the conflict persists and the macro environment deteriorates, high-quality large-cap stocks likely offer the best margin of safety and are currently trading at cheaper valuations than they have in several quarters. It’s difficult to say precisely which direction the macro will go, but we think a balanced equity portfolio can continue to deliver.

Bonds may have multiple ways to win. Rates have moved higher, and spreads have widened, which means you're getting a higher absolute return from fixed income today than you were a few months ago.

If the conflict de-escalates — and early signs suggest that process has begun, even if unevenly — spreads are more likely to tighten from here, which should help bond prices. If we're right that the Fed is at worst going to hold but more likely to cut, that's another potential tailwind for bonds. And of course if the macro picture deteriorates further, we’d expect bonds to resume their traditional role as a portfolio ballast.

If you're underweight fixed income relative to your target allocation, this could be a good time to rebalance.

We’ll learn a lot in Q2. Right now, all eyes remain on the rapidly developing situation in Iran. If the current path of de-escalation holds, that should take pressure off oil prices, ease inflation concerns, and give central banks more room to sound accommodative again.

At the same time, we’ll also begin to hear directly from companies in the coming weeks as they report Q1 results. We’ll get a backward-looking view into the first quarter, but more importantly, we’ll understand whether geopolitical volatility is actually impacting earnings forecasts for the remainder of the year.

Our base case is that de-escalation in Iran continues (even if the path isn’t linear) and earnings estimates hold steady in the coming months. If that happens, Q2 may look a lot more like the first two months of the year than the last.

Disclosure:

This communication is for informational purposes only and does not constitute investment advice or a recommendation to buy, hold, or sell any security. Forward-looking statements involve risks and uncertainties. Past performance is not indicative of future results.

.svg)

.svg)

.svg)