For the first two months of 2026, the global market narrative was relatively straightforward: inflation was cooling, and major central banks across the globe were cutting interest rates.

Our 2026 Outlook was playing out largely as anticipated. Loosening financial conditions were driving a rotation into cheaper, more rate-sensitive areas of the market, including international equities and smaller-cap U.S. stocks.

The recent escalation of the conflict in the Middle East and the resulting spike in oil prices have abruptly derailed that momentum. In just a few weeks, an energy shock has shifted the conversation for most central banks from "when do we cut?" to "should we hike?"

This week, in a rare alignment of the monetary policy calendar, the Fed (U.S.), ECB (European Union), BOE (England), and BOJ (Japan) all held policy meetings within 48 hours of each other.

On a headline basis, there’s still remarkable synchrony across global central banks – the result in every case was "hold.” But beneath the surface, rate expectations are diverging, with broad implications for global portfolios.

The Importer Penalty: Europe and Japan

The differences in how rate expectations have repriced reveal a geographic divide driven largely by energy dependence and the strictness of legal mandates.

Europe (ECB & BOE): Laser-Focused on Headline Inflation

Europe is a major net importer of energy. For the ECB and the BOE, an oil shock is an unmitigated cost increase that feeds directly into headline consumer prices. Importantly, both central banks operate under a "hierarchical" mandate, meaning they are legally required to prioritize price stability (2% inflation) above all other economic concerns. The sudden spike in energy costs leaves them with very little flexibility, forcing them to pivot away from planned rate cuts toward maintaining restrictive policy.

"The war in the Middle East has made the outlook significantly more uncertain, creating upside risks for inflation..." — ECB President Christine Lagarde

"Whatever happens, our job is to make sure inflation gets back to its 2% target." — BOE Governor Andrew Bailey

Japan (BOJ): Stagflation Top of Mind

Japan is exceptionally vulnerable to this geopolitical shock, importing roughly 95% of its crude oil directly from the Middle East. For the BOJ, surging oil prices combined with a structurally weak yen create the potential for a toxic stagflationary dynamic. Because their mandate focuses on price stability in the context of a "sound and functioning economy," the BOJ is hitting the pause button, delaying its long-awaited tightening cycle to avoid breaking a fragile economic recovery.

“The conflict could weigh on the economy by worsening the output gap, thereby pushing down underlying inflation. On the other hand, rising oil prices and the weak yen could affect households' medium- and long-term inflation expectations. If so, that could push up underlying inflation.”— BOJ Governor Kazuo Ueda

The U.S. Exception: Why the Fed Has Flexibility

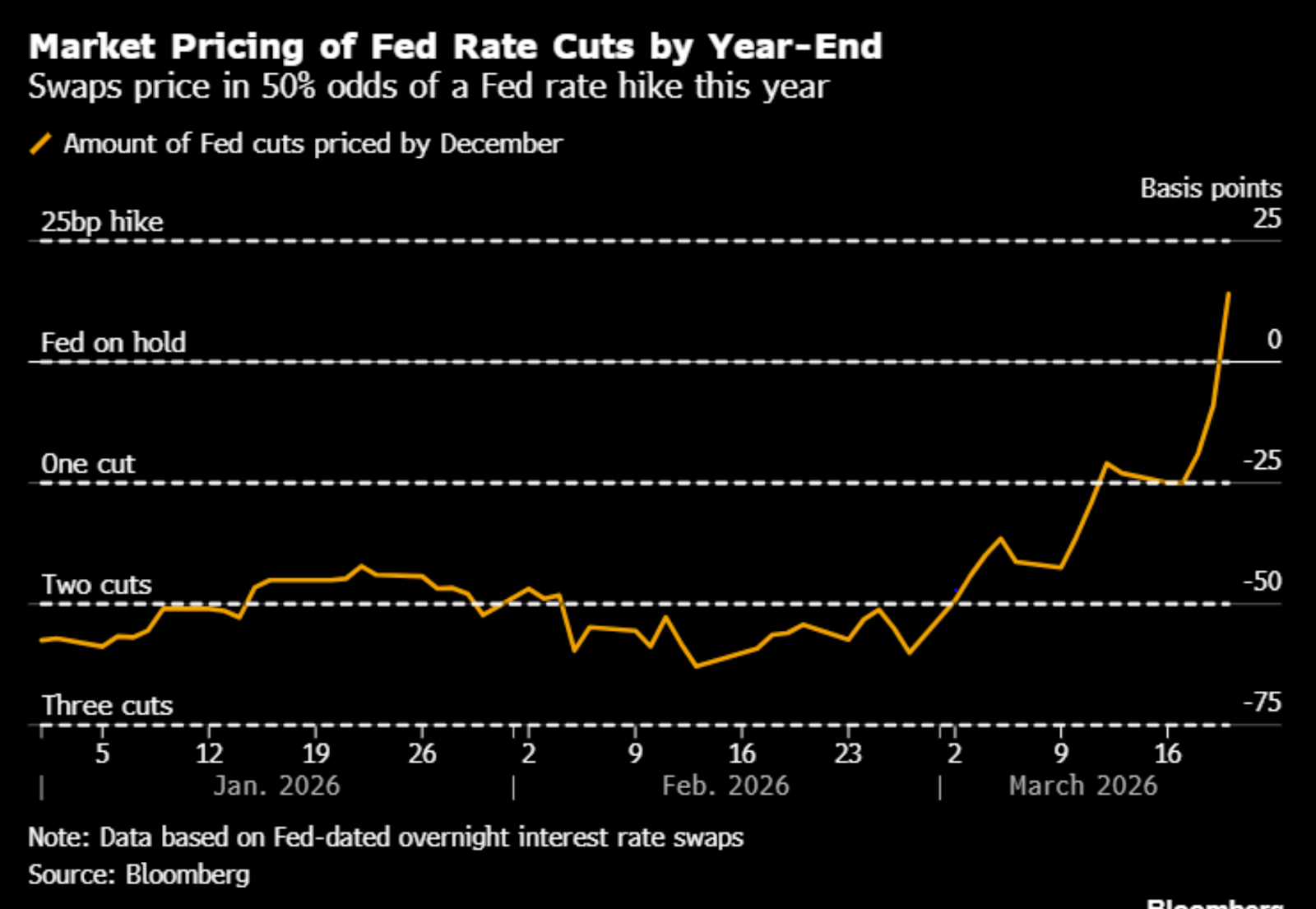

After the Fed held rates steady this week, expectations of rate cuts in 2026 quickly evaporated. By Friday, bond traders began pricing in a 50% chance for a rate hike by the Fed by year-end.

We think consensus is overshooting.

While rate hikes may be more plausible abroad, we believe they are highly unlikely in the U.S., for three key reasons:

- Importer Status: Unlike Europe and Japan, the U.S. is a net energy exporter, providing some buffer for domestic consumers. This dynamic is visible in the current spread between U.S. domestic crude (WTI at $98) and the global benchmark (Brent at $112). Higher energy costs affect consumers everywhere, but this $14 discount offers the U.S. some degree of mitigation against the broader inflationary pressures seen globally.

- Headline vs. Core Inflation: A spike in crude oil immediately drives up headline inflation (the price at the pump). But the Federal Reserve anchors its policy to core inflation, which strips out volatile food and energy prices. Recent estimates from Apollo Global Management suggest that even a sustained, severe oil shock might only add roughly 0.1% to core inflation. It is unlikely the Fed would resume a hiking cycle based on a temporary headline shock that barely moves the core data.

- The Fed’s Dual Mandate: Markets seem to be missing the key vulnerability of a prolonged increase in oil prices: economic growth. Unlike many other central banks, the Fed operates under an explicit "Dual Mandate," giving it the legal flexibility to weigh the inflationary impact of oil against the health of the labor market. If the shipping crisis in the Strait of Hormuz is not resolved soon, oil could spike to extremes. At that point, it stops being solely an inflation story and becomes a demand destruction story. The economic damage of a severe energy spike could automatically cool down the broader economy, essentially doing the central bank's job for them. Ironically, a massive oil shock might actually increase the likelihood of eventual rate cuts if it triggers a severe contraction in U.S. growth.

We believe these structural differences are why the Fed's commentary this week remained much more balanced and significantly less hawkish than its global peers:

"In the near term, higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy." — Fed Chair Jerome Powell

The Bottom Line: Risks to the 2026 Easy Money Thesis

One thing remains clear: if current rate expectations hold, 2026 will be a significantly more difficult environment for markets in all regions than anyone anticipated at the start of the year. The "easy money" trade — predicated on a synchronized cycle of global central bank easing while growth remains steady — is no longer the base case.

The U.S. does possess structural buffers that Europe and Japan lack. Its status as a net energy exporter limits how much an oil spike translates into domestic inflation, and the Fed's dual mandate gives it flexibility that the ECB and BOE simply don't have.

For diversified portfolios, this matters: if the Fed eventually cuts rates, U.S. bond prices would rise, allowing fixed income to act as a meaningful shock absorber against equity volatility.

But these possible cuts would not translate to safe ground: a few months ago, the market was pricing in rate cuts driven by a victorious fight against inflation. Today, we are talking about the possibility of rate cuts due to economic damage that would require Fed intervention. That is a very different destination, even if the interest rate number looks the same.

Disclosure:

This communication is for informational purposes only and does not constitute investment advice or a recommendation to buy, hold, or sell any security. Forward-looking statements involve risks and uncertainties. Past performance is not indicative of future results.

.svg)

.svg)

.svg)