Last week, AI disruption was a tech story. We wrote about software stocks repricing rapidly as investors digested the implications of a new wave of AI tools that could replace tasks once handled by expensive enterprise platforms. The selloff was sharp, but contained.

This week, the market decided that AI disruption is not just a tech problem anymore.

Target Practice

AI fears tore through sector after sector of the economy—each triggered by an AI product launch (or the expectation of one).

In the span of five trading days, billions in market value were erased from industries that had nothing to do with software.

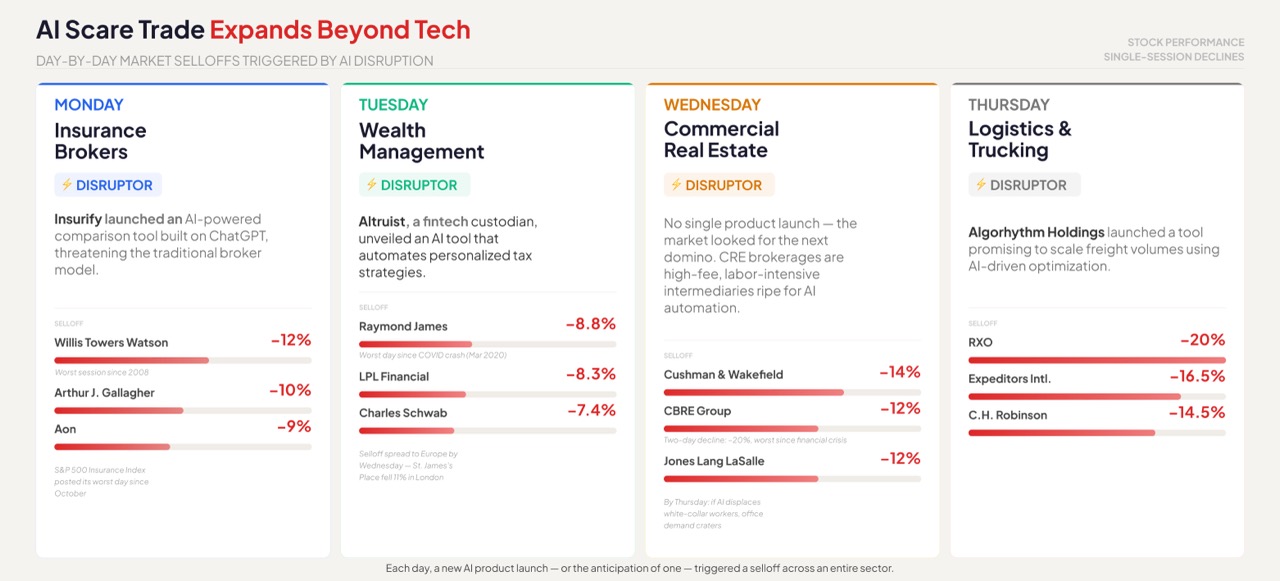

Monday: Insurify’s ChatGPT-powered comparison tool triggered a selloff in insurance brokers, with Willis Towers Watson posting its worst session since 2008.

Tuesday: The contagion jumped to wealth management after Altruist, a custodian for RIAs like Range, unveiled an AI tax-strategy tool, sending Raymond James to its steepest decline since the COVID crash.

Wednesday: Commercial real estate services cratered without any specific catalyst. The market had begun extrapolating — if AI could displace insurance brokers and financial advisors, the high-fee, labor-intensive world of CRE brokerage could be next. CBRE’s two-day decline hit 20%, its worst since the financial crisis.

Thursday: Freight and logistics joined the sell-off after Algorhythm Holdings demoed an AI optimization tool, with truck-broker RXO dropping 20%.

In four sessions, the “AI scare trade” evolved from a narrow disruption story into a broad referendum on the future of white-collar intermediaries. The common thread: these are businesses that sit between buyers and sellers, extracting fees for expertise that AI can now automate at a fraction of the cost.

The Knowledge Premium Breaks Down

The market doesn’t expect an AI tool launched on a Tuesday to replace every financial advisor or insurance broker by Friday. The fear is about the economic structure of these businesses. Industries like insurance brokerage, wealth management, and commercial real estate services share characteristics that make them vulnerable:

- Information asymmetry → high margins. These are businesses where the provider knows more than the customer, and charges accordingly. AI compresses that gap.

- Human labor as the moat → barriers to entry. For many of these businesses, talented human capital has been their competitive advantage. If the “rainmaker” becomes less important to delivering value, the talent premium erodes, along with a barrier that keeps competitors out.

- Entrenched fee structures → decades of stable pricing. The 1% AUM fee, 6% real estate commission, insurance brokerage spread — these have been remarkably durable. But the market is questioning what happens to legacy pricing when the cost of delivery meaningfully declines.

Investors are asking a simple question: if AI makes the work cheaper to produce, how long before consumers pay less for it? When technology drives down the cost of delivery, prices eventually follow.

Incumbents will argue they can adopt AI to cut their own costs while holding pricing steady. That’s the bull case. But businesses rarely capture all the economic value from a technology shift — consumers eventually get their share. And if the legacy players don’t offer it willingly, a startup or a competitor will.

What’s Keeping the Market Afloat?

While intermediary-heavy sectors bled this week, other parts of the market had a very different experience.

AI Infrastructure

While the market debates which industries AI will disrupt, the bet on the infrastructure behind it remains firmly intact.

Energy remains the best-performing sector of 2026, up roughly 21% year-to-date. Data center operators like Equinix jumped 10% on the same Thursday that the S&P 500 fell — the market’s way of saying it still believes in the buildout, even as it reprices the companies on the wrong side of it.

Defensive Industries

Investors are also parking capital in businesses with tangible products and predictable demand — companies that don’t sell human expertise and aren’t exposed to fee compression.

Consumer staples and utilities led the S&P 500 on Thursday, with companies like Walmart and Coca-Cola showing gains.

Broader Rotation to Value

“Cheaper” stocks with lower P/E multiples are significantly outperforming their expensive counterparts.

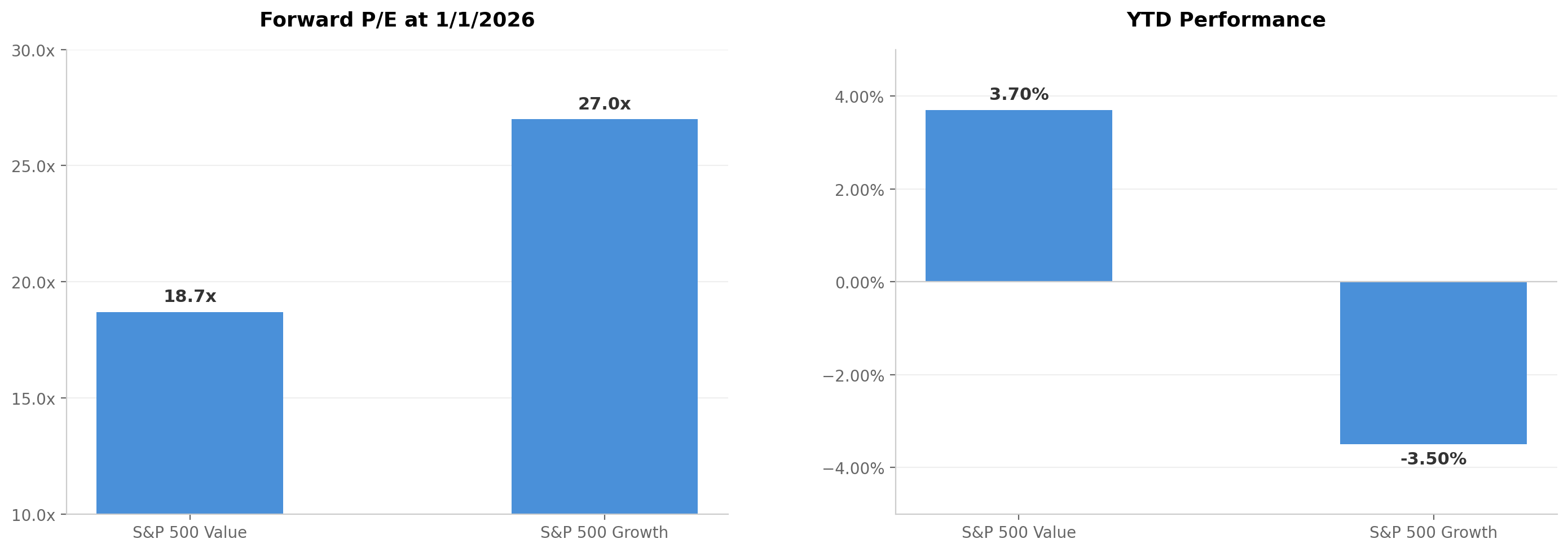

The S&P 500 Value Index, which traded at ~19x forward P/E at the beginning of the year, is up about 3.7% year-to-date. The more expensive S&P 500 Growth Index, which traded at 27x to start the year, is down roughly 3.5%. That’s a 7-point gap in six weeks — a significant reversal from growth’s dominance over the past several years.

The companies hit hardest right now are those with the most to lose—high margins, premium pricing, and high fee structures. AI threatens to compress all of that. The market is correcting these valuations today, long before the impact ever shows up in an earnings report

But what about companies on the other end of the spectrum? Businesses with thin margins, high cost structures, and limited pricing power — the kind that analysts already describe as needing to “grow via cost cuts” — might actually have the most to gain from an AI productivity shock.

In some ways, AI is acting as an equalizer. Competitive moats that were built over decades through proprietary data, entrenched client relationships, and sheer complexity of the work are becoming less impenetrable. That’s a problem if you’ve been charging a premium for those advantages. But it’s an opening if you’re an innovator or looking for a second chance to compete.

Two Takeaways

Valuation matters again.

Growth stocks have dominated for the better part of 15 years. With only brief exceptions in 2016 and 2022, paying up for the fastest-growing companies has been a winning strategy regardless of price. That trade has started to reverse. When the future is uncertain, investors tend to seek a margin of safety. They gravitate toward businesses where they’re paying less for each dollar of earnings, and where there’s less air to come out of the valuation if the thesis breaks. Right now, what you pay matters as much as what you own.

The pressure to adapt is universal.

Investors are re-underwriting business quality across sectors. High-margin intermediaries will need to prove they can adopt AI without surrendering the pricing that made them profitable. Lower-margin operators arguably have the most to gain, but will need to show they can actually innovate, capture productivity benefits, and translate them into better economics.

For all companies, standing still is not an option. The market has made the cost of complacency very expensive, very fast.

This communication is for informational purposes only and does not constitute investment advice or a recommendation to buy, hold, or sell any security. Forward-looking statements involve risks and uncertainties. Past performance is not indicative of future results.

.svg)

.svg)

.svg)