Software stocks are in freefall. The iShares Software ETF (IGV) is down over 20% year-to-date and nearly 30% from its September peak—its fastest drawdown since the financial crisis. Before Friday’s bounce, the S&P 500 Software & Services Index had fallen for eight consecutive sessions. Over $1 trillion in market value has evaporated since January 27.

iShares Software ETF Price Performance

I spent the week talking to former colleagues on the hedge fund side. The atmosphere was decidedly grim. These conversations made it clear that this doesn't feel like a normal pullback.

Fund managers are operating with a “get out first, ask questions later” mindset. They aren't analyzing individual software names—they're selling the sector wholesale in response to painful muscle memory. They've seen structural shifts destroy industries before, and pattern recognition is triggering a rapid repositioning in portfolios.

It’s AI, What Else?

What’s driving the aggressive selloff? AI has been the market's rising tide for three years. But tides don't lift every boat.

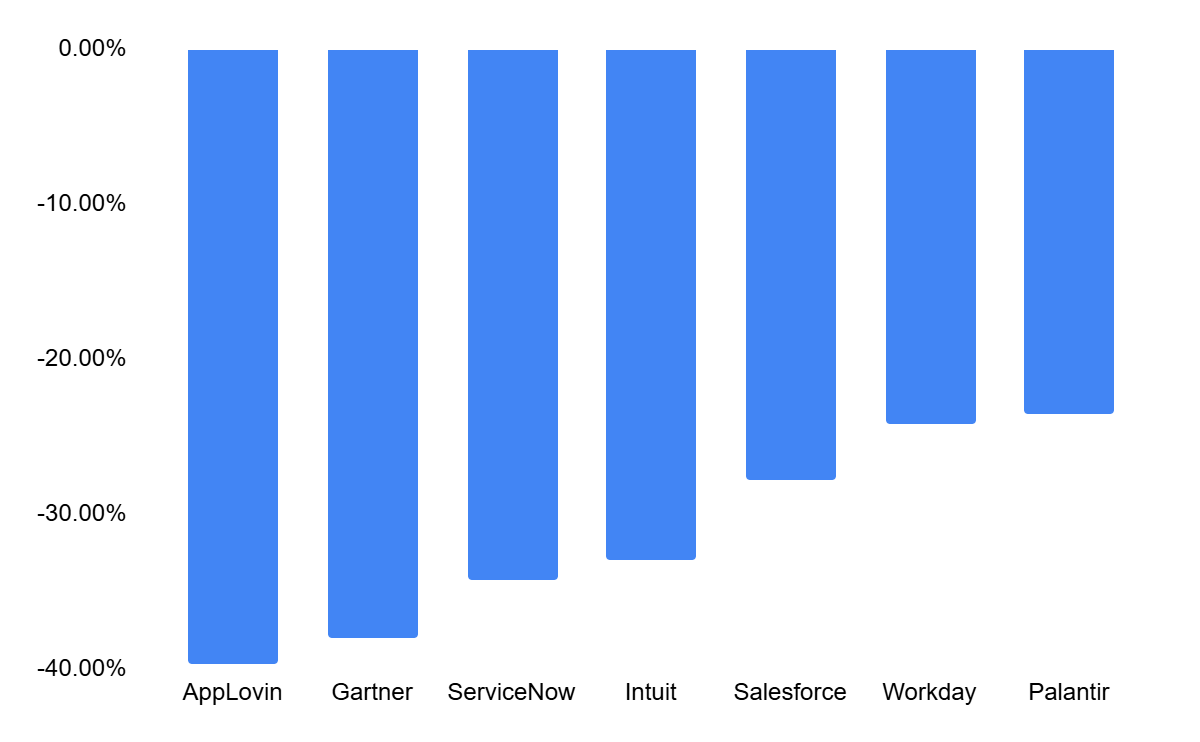

Private AI companies—some now worth in the hundreds of billions—are releasing products that directly compete with incumbent software. This week, Anthropic's Claude launched enterprise plugins targeting legal research, contract review, and compliance workflows—going head-to-head with the exact services that underpin Thomson Reuters' $7 billion+ revenue base. In response, Thomson Reuters dropped 16% in a single session—its largest intraday decline on record.

Thomson Reuters was just the first domino. Investors started asking: if legal software is vulnerable, what about CRM? HR? Financial data? Anxiety around software that was already developing over the past several months spread across sector heavyweights—companies spanning everything from tax software to cloud infrastructure to enterprise sales tools.

Software Stock YTD Performance

Back to Fundamentals

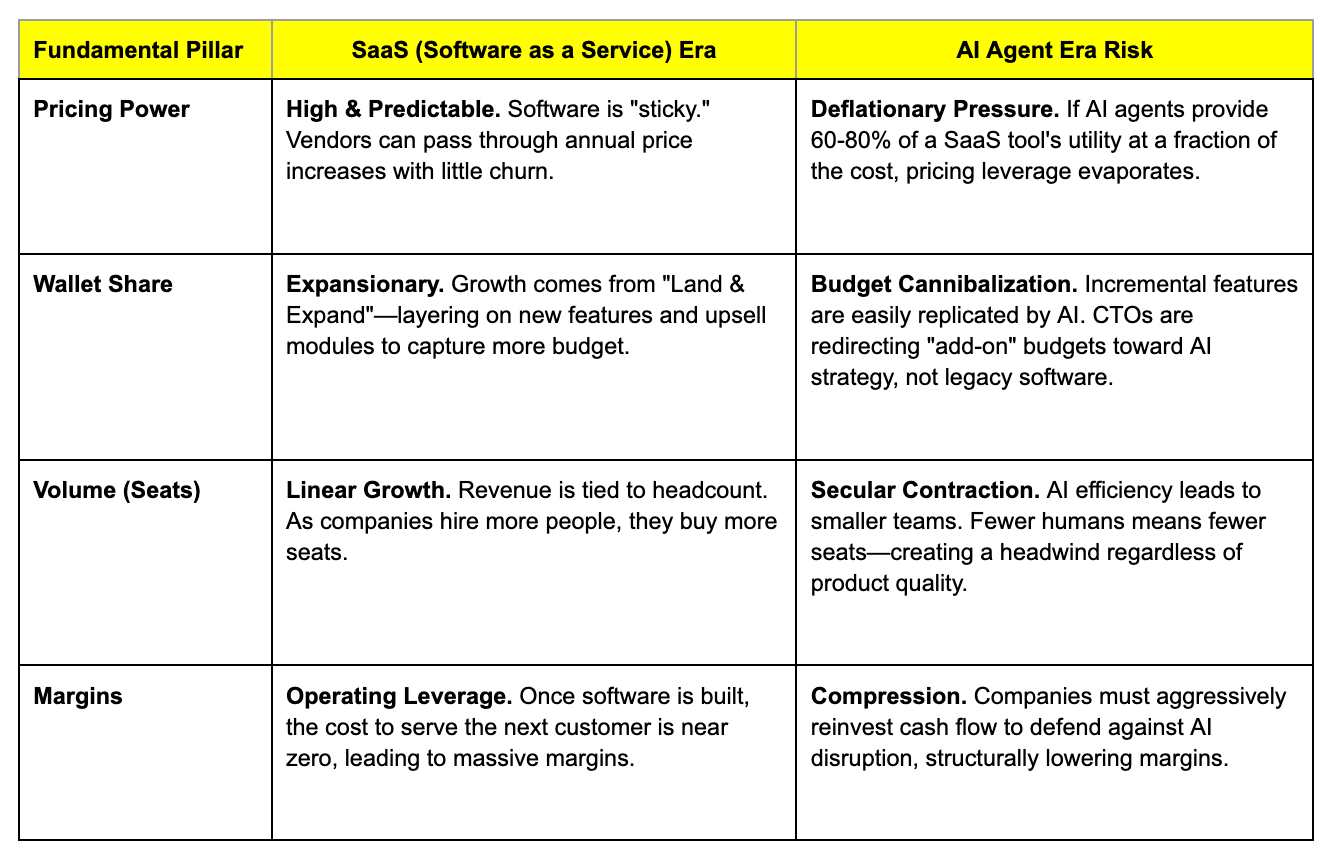

If you’ve been reading Range’s content, you know we always come back to fundamentals. Short-term market moves can be driven by technicals and fund flows. But long-term market dynamics are usually guided by movement in earnings, balance sheets, and valuation multiples.

For the last decade, software stocks have traded at a massive premium to the overall market (measured by their forward P/E valuation), and for good reason. They’ve exhibited strong pricing power, excellent growth, and healthy margins.

But now the market is asking if each of these pillars is under threat simultaneously.

We believe investors have been paying 25x–30x earnings for software because it was viewed as the ultimate "safe compounder"—predictable growth with minimal existential risk.

When that safety is questioned, the multiple can meaningfully reset. The market is currently trying to find the new "floor" for software multiples. If the sector de-rates from a "Growth" multiple (30x) to a "Market Average" multiple (17x), stock prices can fall further even if earnings remain flat.

S&P 500 Comparison: Software vs Equal-Weight

Is This the New Cable?

The historical analogy that keeps coming up in my conversations is media and cable between 2010-2020.

Cable subscriptions peaked in the early 2010s. The "cord-cutting" thesis was initially dismissed. Then pay TV penetration dropped 20% over the next decade. Ad revenue fell to its lowest since 2007. Companies that seemed invincible—massive subscriber bases, decades of content, entrenched distribution—saw their businesses structurally erode. Profits didn’t go away overnight, but media stocks never recovered to their prior valuation range.

The potential parallel to software is uncomfortably close. At the more extreme end of the spectrum, some on Wall Street are comparing software to print media or department stores—industries where disruption didn't just compress multiples but put a large swath of businesses in bankruptcy. We think that's too bearish for the best enterprise software businesses. But the cable analogy—where companies survived but stocks permanently derated—is a plausible bear case for the sector.

Our View

The fundamental questions about growth, margins, and pricing power are real and won't resolve quickly. Structural shifts—as we saw in the media sector—can be deeper and longer than most investors expect.

That said, liquidation has become indiscriminate. We are seeing high-quality payments, cybersecurity, and infrastructure providers—whose products are mission-critical and unlikely to be vibe-coded—sold in lockstep with companies that are genuinely in AI's crosshairs. The market is currently disposing of 'software' as an asset class, rather than distinguishing between winners and losers. This behavior typically creates opportunities—but discipline and selectivity are important. Even a great house loses value when the neighborhood goes bad.

Despite all the carnage, portfolios diversified beyond tech are showing resilience. The S&P 500 is still up 1% year-to-date. Energy, industrials, and materials are leading the market while technology is the worst-performing sector. The Russell 2000 is up nearly 8%. International stocks have gained 7-8% across developed and emerging markets.

The broadening we discussed in our 2026 Market Outlook is playing out in real time—just not gracefully.

This communication is for informational purposes only and does not constitute investment advice or a recommendation to buy, hold, or sell any security. Forward-looking statements involve risks and uncertainties. Past performance is not indicative of future results.

.svg)

.svg)

.svg)