Sophisticated Wealth Management. Intelligently Connected.

Combining the sophistication of a traditional advisor with the automation of a modern robo to seamlessly coordinate your investments, planning and taxes.

SEC-registered fiduciary · Flat fee¹ · No commissions

A disciplined approach, built to seek to grow wealth over the long term.

Investments at Range don't live in a silo — they're managed alongside your taxes, cash flow, and goals.

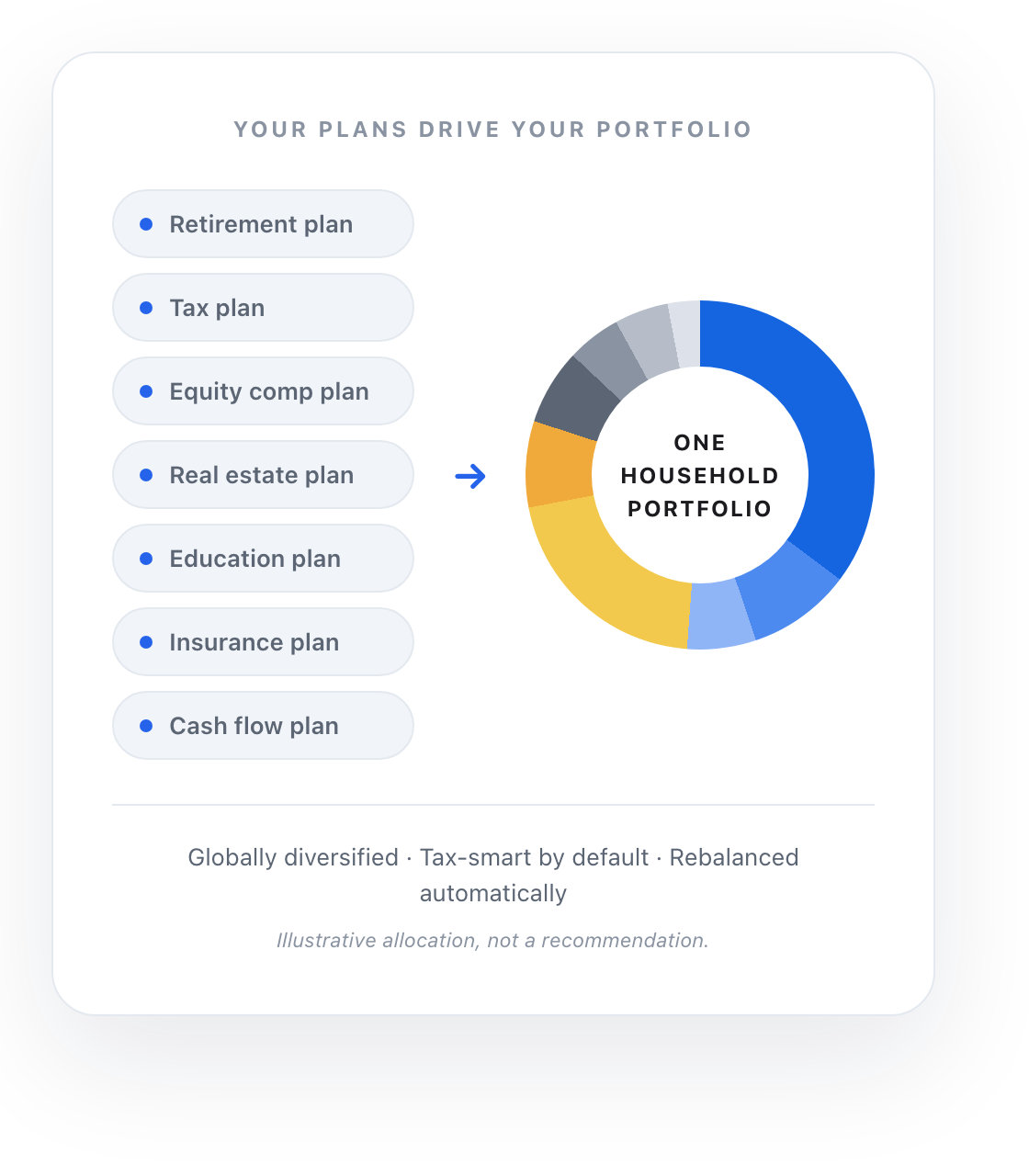

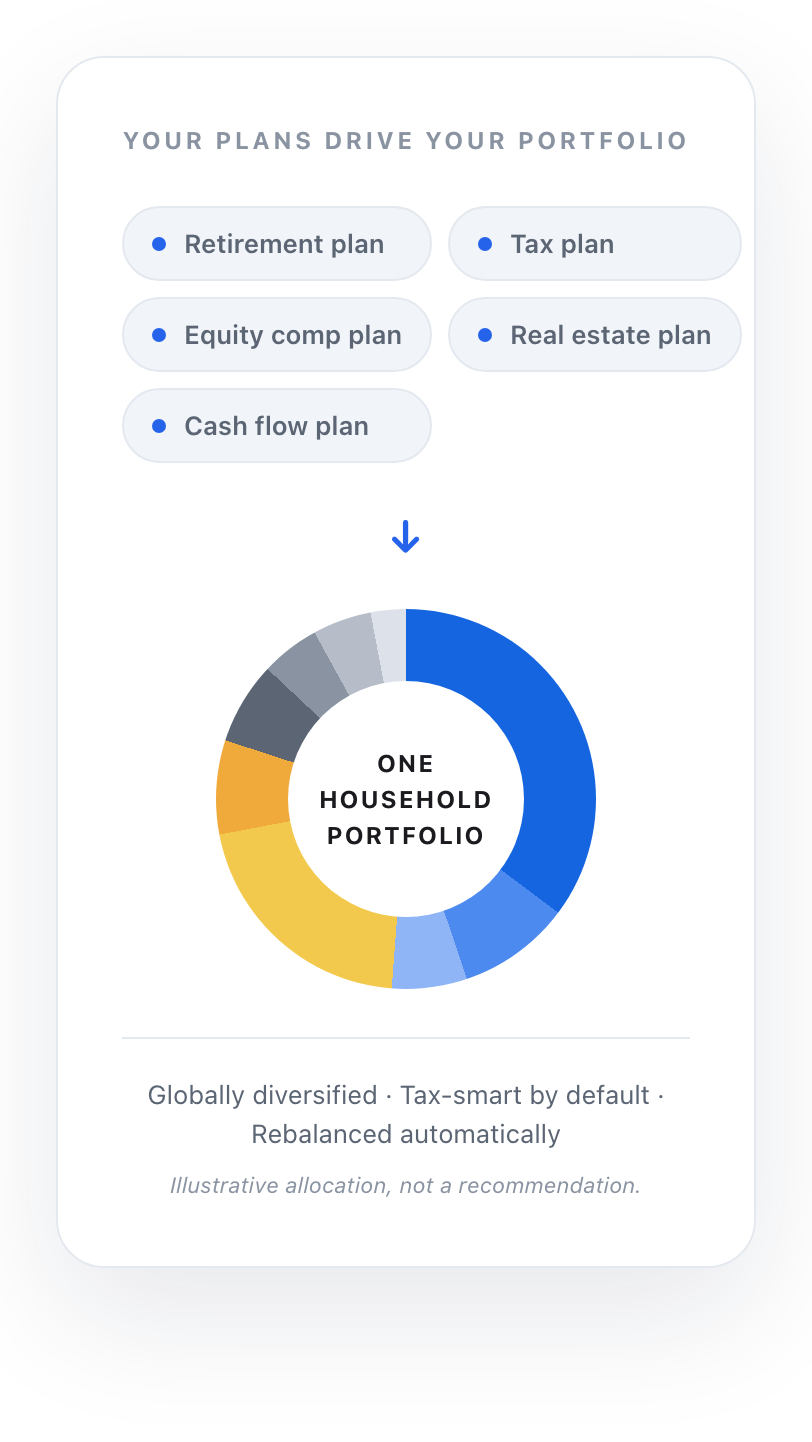

Integrated portfolio management

We treat the household, not the account, as the unit of investment. Allocation, asset location, and trading are coordinated across both spouses and across the accounts we manage and those we don't.

Evidence-based investing

We utilize low-cost, globally diversified core portfolios designed to be resilient across market cycles. We tailor these portfolios to each household's specific goals, constraints, tax situation and liquidity needs.

Compounding what we can control

Markets move on their own schedule. Fees, taxes and behavior we can manage. We focus where consistent attention has the most impact: lower fees, tax-aware asset location, tax-loss harvesting and disciplined rebalancing.

Six pillars that define how Range invests.

The sophistication of a traditional advisor with the automation of a modern platform — seamlessly coordinating your investments, planning and taxes.

Zero AUM fee¹

Most advisors charge about 1% of everything you've invested with them, every single year. We don't.

On a $1M portfolio, a 1% AUM fee is $10,000 a year — and it grows as your portfolio grows. Range doesn't charge on assets, because growing wealth shouldn't be penalized.

Third-party fees may apply and typically range from 0–22 bps.¹

Whole-household optimization

We don't manage one account in a vacuum. Your full financial picture is the unit we plan around.

Both partners' 401(k)s, HSAs, IRAs, and taxable brokerage accounts are managed as one coordinated portfolio — eliminating duplication, overlap, and gaps.

Integrated with planning

Investing is connected to taxes, retirement, equity comp, and your household's actual goals.

We execute customized portfolio transitions, initiate backdoor Roths, align capital gains budgets with tax projections, and rebalance for life events — coordinated by one team.

Tax-smart by default²

Smart tax decisions are baked into how we run the portfolio every day, not bolted on in December.

Daily scanning for tax-loss harvesting opportunities, direct indexing, strategic asset location across account types, in-kind ACAT transfers, and automated rebalancing that incorporates customized capital gains budgets.

Built for volatility

Evidence-based portfolios designed to hold up across market cycles. No emotional timing.

We invest for the long run. Portfolios are globally diversified across regions, sectors, and asset classes — with no short-term market chasing. Automated rebalancing and tax-loss harvesting respond systematically to market moves.

Fiduciary DNA

We're legally required to put the member's interest first. Always.

SEC-registered RIA. No commissions, no hidden markups, no kickbacks from product issuers. The only money we make is the flat membership fee you pay — so our incentives line up with yours.

Our edge is what we can control.

Range creates differentiated value through the parts of investing that are controllable: taxes, fees, rebalancing discipline, transition planning, and avoiding avoidable mistakes.

Selling investments that are down to capture a tax loss, then buying similar ones so the portfolio stays invested. We scan for opportunities daily, throughout the year — not just in December.

Placing each asset type in the account where it's taxed most efficiently — allocating across taxable, tax-deferred, and tax-free accounts as one portfolio.

Moving into your target portfolio on a tax plan, not an expedited timeline. We set an annual realized-gains budget aligned with your tax projection and pair rebalancing trades with harvested losses to stay inside it.

No emotional timing. No short-term market chasing. Automated rebalancing and tax-loss harvesting respond systematically to market moves — and your advisory team is there when headlines get loud.

No AUM fee. Low-cost, broad-market index ETFs at the core. Institutional direct indexing passed through at the custodian's rate with no markup.

Automated rebalancing keeps your portfolio aligned to its target allocation — and incorporates your capital gains budget, so staying balanced doesn't create a surprise tax bill.

RSU vests, Roth conversions, large purchases, and life events flow directly into portfolio decisions — because planning and investing live on one team.

Instant, around-the-clock access to your portfolio via RAI — immediate answers on rebalancing, exposures, and contributions whenever you need them, alongside your human advisory team.

What this is worth in dollars.

These controllable levers are not abstract — they can translate into measurable after-tax dollars for members.

On a $1M portfolio at an 8% baseline return, this can translate to roughly $500K–$1.4M in additional accumulated wealth over 10 years.³

Disclosure: assumes a high-tax-bracket investor.⁴ Illustrative ranges, not guaranteed.

Value of Range figures are based on the following sources:

- NerdWallet, “How Much Does a Financial Advisor Cost in 2026?”

- ICI Research Perspective, Trends in the Expenses and Fees of Funds, 2025. March 2026 // Vol. 32, No. 1.

- Financial Planning, “Vanguard Advisor's Alpha study cites tax-loss harvesting.”

- Vanguard, Revisiting the Conventional Wisdom Regarding Asset Location, August 2022.

- Vanguard, “Investors winning as a behavior gap shrinks.”

- JPMorgan, “How cutting edge technology can enhance your wealth with tax savings,” June 2025.

See how Range would manage your household.

A consultation with our team walks through your accounts, your tax picture, and what a coordinated portfolio would look like.

Schedule a ConsultationHow your portfolio gets built.

A disciplined, four-step process — from your whole household down to the personal details that make the portfolio yours.

The whole portfolio, working together

Both partners' 401(k)s, HSAs, IRAs, and taxable brokerage accounts are managed as one coordinated portfolio — eliminating duplication, overlap, and gaps.

Move what you want. We coordinate around everything else.

Some accounts we manage directly. Others we advise on and coordinate with. Together they make up one household portfolio.

We start with a disciplined core portfolio

Range starts with a disciplined core portfolio designed to give every member a strong investment foundation — low-cost, globally diversified, and built from broad-market index ETFs. No stock picking. No market timing.

Illustrative allocation for educational purposes only — not a recommendation. Actual portfolios are customized to each household's goals, constraints, tax situation and liquidity needs, and may differ materially.

Then we tailor it to your household

Every member starts with the disciplined core, then we customize it to your financial life — appreciated securities, employer stock, concentrated positions, capital gains budgets, and compliance restrictions. The core stays consistent; personalization is what bends it to fit.

A member with concentrated employer stock from RSU vests

The core stays disciplined. We can replace the standard large-cap exposure with a direct indexing sleeve that excludes the employer's stock to offset the concentration — reducing single-stock risk and unlocking tax-loss harvesting at the individual holding level, while the rest of the portfolio stays the same.²

What Range does that the rest of the category doesn't.

Seven things Range Investment Management does that others do not, or do inconsistently.

Household-level optimization

Automated platforms optimize accounts they custody. AUM-fee advisors optimize what they are paid on. Range treats the entire household as one portfolio across taxable, retirement, equity comp, and held-away accounts.

Structural fee alignment

With no AUM fee,¹ our advice on 401(k) rollovers, asset location, and consolidation is not biased by what we get paid on. Our economics line up with yours.

Planning and investments in one team

RSU vests, Roth conversions, large purchases, and life events flow directly into portfolio decisions — coordinated by one team, not handed off between firms.

Backdoor Roth and account retitling, executed for you

Done on members' behalf by the investment team — not a checklist you're left to complete on your own.

Institutional direct indexing, no markup²

Daily, algorithmic tax-loss harvesting at the lot level. The same functionality typically costs 25–75 bps at well-known platforms. Range passes through the custodian's institutional rate of 12–22 bps with no markup.

An annual capital gains budget, enforced through rebalancing

We set a realized gains budget each year, aligned with your tax plan, and pair rebalancing trades with harvested losses to stay inside it — systematically, not sporadically.

24/7 AI-powered insights⁵

Instant, around-the-clock access to your portfolio via RAI — immediate answers on rebalancing, exposures, and contributions whenever you need them, alongside your human advisory team.

Five things to remember.

Put a professional team in charge of your portfolio.

Range membership is a flat annual fee — our most popular Platinum tier is $5,950 per year, no matter how large your portfolio grows.¹ Investment management is one part of a complete plan across taxes, equity comp, estate, and retirement.

Schedule a ConsultationSEC-registered fiduciary · Custody at Altruist · No commissions or product kickbacks